2015年04月24日時点

While headline durable goods orders were up an impressive-looking 4.0% in March, all that gain came in the volatile transportation equipment component. Net of transportation equipment, durables orders were down 0.1%. Though a -0.1% move in “underlying” durables orders doesn’t sound bad, it marks the sixth straight decline in this aggregate.

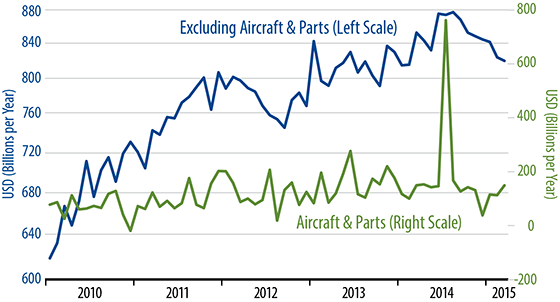

The main driving factor within transportation equipment is nondefense aircraft, and as you can see from the green line in the accompanying chart, even the sharp March gain there leaves aircraft orders barely at the average levels of the last five years. In other words, aircraft manufacturing activity is not rising, and other durables manufacturing sectors have been contracting recently.

Capital goods orders excluding aircraft are shown by the blue line in the chart, and this indicator is more or less a microcosm of durables activity in general. Here, orders dropped in March for the seventh straight month.

Again, factory activity had already been softening for a number of months, and we learned earlier this month that factory payrolls and industrial production in March were soft. So, today’s news is not a surprise, but neither does it provide any counter to the recent string of bad news coming out of the manufacturing sector.

Factory activity has clearly weakened over recent months, while homebuilding showed some signs of life at the turn of the year, before stumbling lately. How these two sectors play out will determine how underlying US growth moves this year. Slower factory growth opposite no change in housing would mean a substantial slowing in US growth, while a favorable turn in both would push underlying growth higher than the 2.0%–2.5% rut in which we have been stuck.

Today’s factory sector data confirmed that this sector remained in its funk through March. Meanwhile, the housing news for March was mixed at best. We’ll see in the weeks ahead whether spring brought better activity to either of these pivotal sectors.