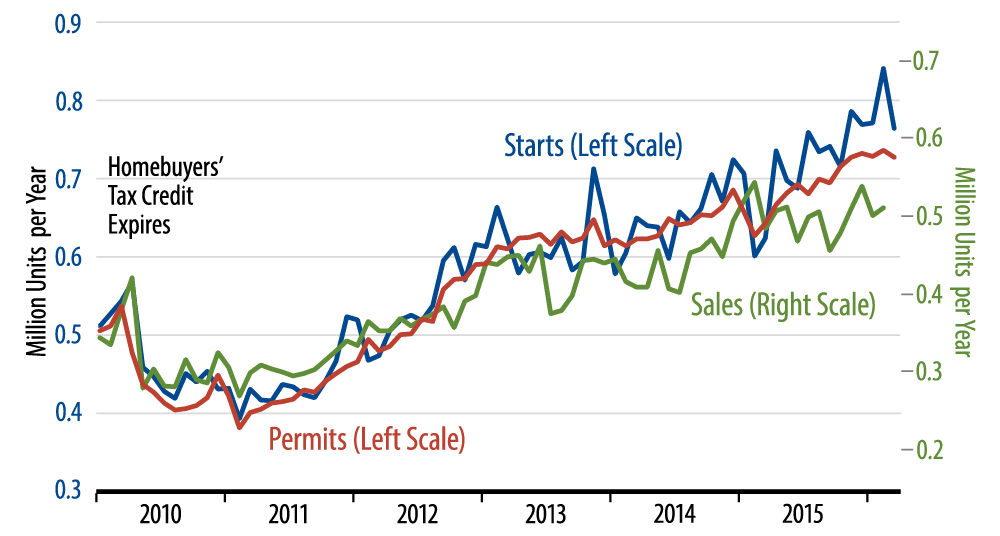

Housing starts declined 8.8% in March, about offsetting a 6.9% (revised up) February gain. The more important single-family starts number declined 9.2% in March, also about offsetting a 9.1% increase in February. The comments we have seen this morning lament these declines as showing disappointingly weak activity. Our take is that the March starts declines are more likely merely random noise within an apparently continuing uptrend in homebuilding activity.

As seen in the accompanying chart (blue line), the swings in single-family starts over the past 2 months are right in line with observed month-to-month experience. Despite the March declines, March starts levels were at worst even with the levels of the past 5 months and well above year-ago levels. As scary as a 9.2% 1-month decline might sound, it is within the Census Bureau's ±10.3% band for common month-to-month swings.

We say this even though our own forecast has been for housing starts to level off. Our view has been that the supply of new homes has gotten way ahead of demand ever since early-2014 and that with inventories of unsold new homes piling up, builders would eventually have to rein in production levels. So far, there is no real sign of this happening. Then again, that pesky flatness in new-home sales remains, even as homebuilding rates continue to rise.

Granted, our take is very different from the Wall Street consensus. The mantra there is that builders are not keeping up with demand. But if that is the case, why do new-home sales levels continue flat opposite rising homebuilding rates and why do inventories of unsold new homes continue to rise?

Obviously, there are different ways to interpret the data. While today's starts and permits news disappointed most analysts, they are not really indicative of weakness in the housing sector. Manufacturing and mining are where the problems lay in the current US economy.