The weakness narrative intensified last month when February showed very weak payroll jobs growth. Our contrary take was that there is always a lot of random fluctuation in the economic data, especially around the turn of the year, and the weak February jobs print came on the heels of especially strong prints for December and January. On average, job growth has been just fine.

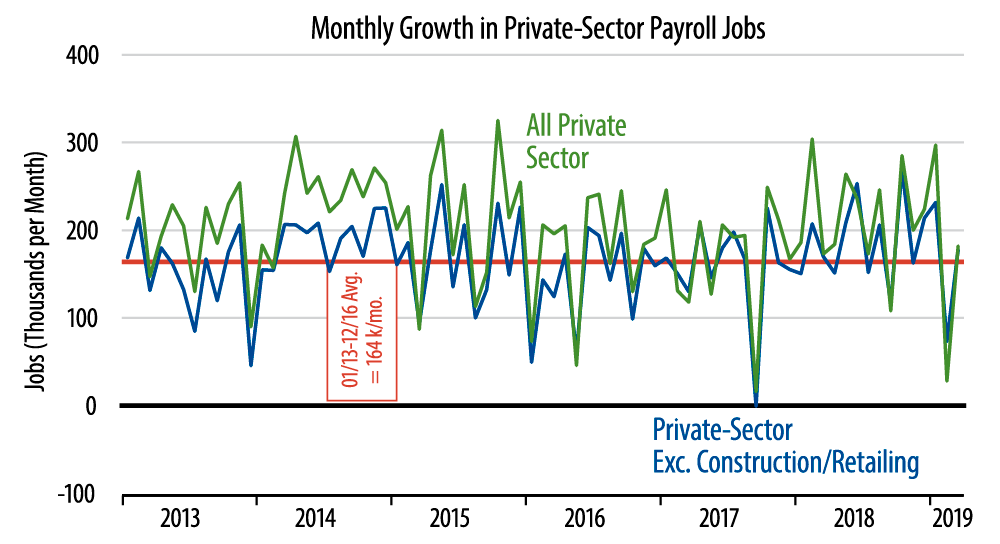

Hopefully, today’s news will quash the recession narrative...at least for a while. Private-sector payroll jobs rose by 182,000 in March, with a slight revision of -8,000 to the February level. For our more reliable job gauge, private-sector less construction and retailing, the March gain was 178,000, with a +2,000 revision to February’s level.

The 178,000 gain for our preferred measure compares to a 164,000 per month average over 2013-16. For the last six months as a whole, average gains were 188,000, well above that average. Even for the last three months—allowing the weak February print to have more play—the average gain is 161,000, essentially right at the average for 2013-16.

In other words, apart from the month-to-month random chop in the data, job growth has continued right at the "norms" of this expansion, if not faster. The recent claims of weakness are just as inapt as were the claims of overheating a year ago.

We abstract from construction and retailing in our analysis because of the extreme volatility they show, especially around the turn of the year. Both construction and retailing jobs softened a bit in recent months, but that only offsets relatively strong jobs data for these sectors a few months earlier. It is always difficult to seasonally adjust these industries correctly, and our guess is that payroll trends in both are quite steady beneath the month-to-month chop.

The one meaningfully soft element of the jobs data recently is in manufacturing, where jobs declined a bit in March on the heels of some downward revisions to January and February. Even here, this is merely what we were expecting, as a softening in exports and—perhaps—capital spending have presaged softer growth in manufacturing. Even here, however, the recent factory sector data are still better than what we saw over 2013-16, just not as strong as in 2017-18.

All in all, it looks as though the economy has moderated enough to justify the Fed’s "pause," but not enough to ratify recession fears. Spring is here, Goldilocks!