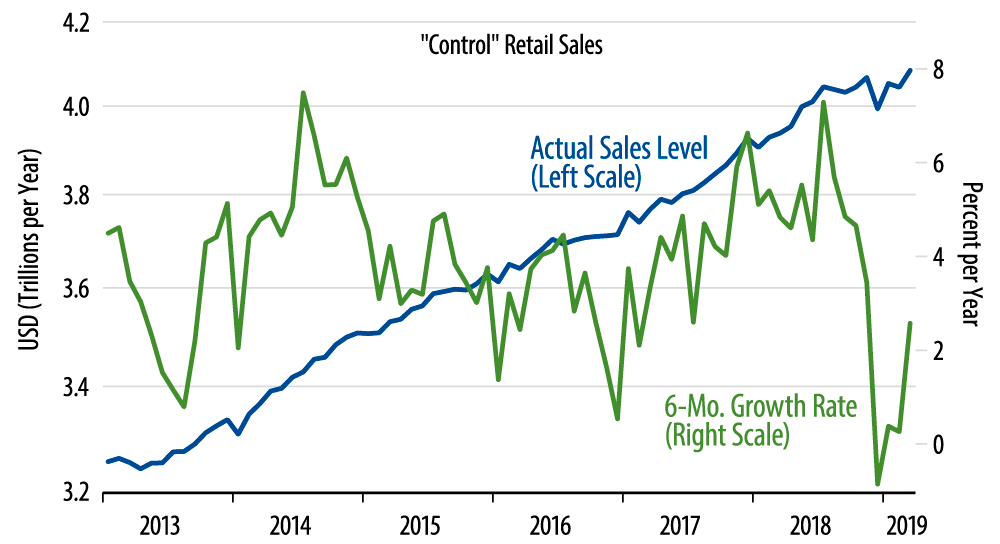

No, the consumer is not surging. All the March gains did was bring sales back to the modest-growth trend line they had been on prior to the Christmas holiday season. You can draw your own trend line through the sales data for the last few years (blue line in chart). To my eye, any trend line you draw that accurately portrays sales in 2017 and early-2018 is going to have a March 2019 level right at or even above the actual sales level for March.

You reach the same conclusion looking at the six-month growth rate also plotted in the chart. Those large March sales gains were enough to bring the six-month growth rate back to all of...2.6%, quite a bit slower than the trend growth rates seen through most of the last two years.

Recall that after a buoyant November sales gain, sales were quite weak in December. We did not take that decline as a sign of grim times ahead for consumer spending. Rather, we thought merely that early Xmas season promotions had pushed sales from December into November, so that sales would rebound in subsequent months. Another polar vortex this past winter may have prolonged the process, but, again, these strong March gains serve merely to bring sales back to pre-holiday trends, almost fully offsetting the December weakness.

What does it all mean for the economy and the Fed? Well, hopefully, these data will kill the recession story for a while. Services consumption spending—not included in retail sales—has held up throughout the last six months, and goods consumption—as reflected by retail sales—is mostly now back on track. Our 2.00%-2.25% GDP growth forecast for 2019 is looking fine.

Meanwhile, there is nothing in these data to contravene the Fed’s latest pause. Again, today’s sales gains merely quash the consumer-is-weakening narrative. There is no strength here per se. With 2019 GDP growth still likely substantially slower than what we saw in 2017-2018 and with inflation subdued, it still looks an imminent rate hike is not in the cards.