2014年4月14日時点

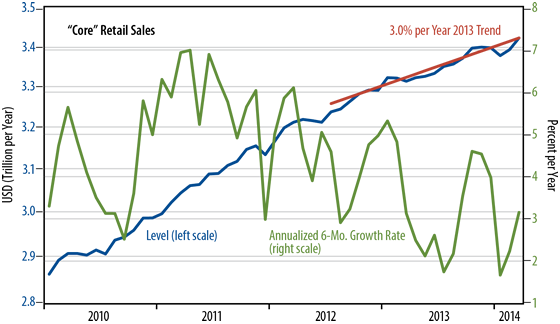

When February retail sales data were released, we pointed out in “By the Numbers” that because January/February data were pulled below-trend by severe winter weather, sales in March and after would have to rise above-trend merely to sustain the soft sales trends of 2013. Because shoppers could not get to stores during the polar vortex, home inventories were depleted, and those inventories would have to be rebuilt by higher-than-normal purchasing once the blizzards subsided.

This pattern was reflected in today's release of March retail sales. Sales in the widely followed "control" measure rose 0.9% in March. Along with modest upward revisions to February, that allowed sales levels to re-attain the 3% per year trend line in place across 2013. In other words, even a 0.9% monthly gain is not much when it was preceded by sharp declines such as those we saw in January.

Notice also that with sales barely back at trend, this wasn’t enough of a rebound to allow any actual restocking of household inventories. So, we are likely to see another "apparently" large sales gain in April in order to allow such restocking, and, again, merely to sustain a 3% growth trend on an ongoing basis.

Contrary to the market consensus, our view is that retail sales—and consumer spending in general—will not show any acceleration this year. While we acknowledge that the apparent January softness was weather-driven, our point is that the apparent March strength is also merely a weather effect. Furthermore, even a similarly large gain next month would be merely a rebound from winter restraints, not a sign of faster sales growth on an ongoing basis. This is the historic pattern we have seen during past blizzards, and it is being repeated presently.