If you didn’t hear, amid all the headlines concerning the Brexit vote, May durables goods orders today were weaker than expected, with total durables orders dropping 2.2% and orders excluding (especially volatile) transportation equipment down 0.9%. Capital goods orders were down 0.8% and down 0.7% excluding aircraft.

We’re not sure why these data were a surprise to the markets, as they are merely of a piece with prior data for May on factory payrolls and industrial production, which also showed declines. Consensus opinion had been calling for a spring rebound in US manufacturing activity, based on the premise that previous weakness was due to a strengthening dollar and declining oil prices, and that both of these trends had stabilized lately. Our contrary take has been that factory-sector softness was much longer-lived than adverse exchange rate and oil price trends, and that it would continue despite the stabilization in oil and the dollar.

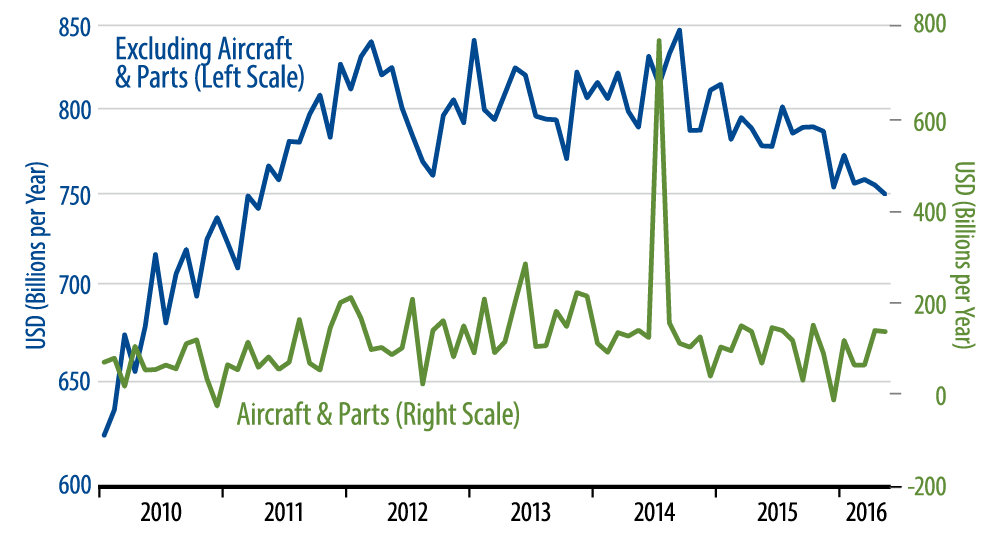

Notice in the accompanying chart that softness in capital goods orders dates back to early-2012, more than 2 years before the onset of a strengthening dollar and falling oil prices, and this is true for most other manufacturing indicators as well. April news had been slightly positive for manufacturing, but the May data have moved uniformly in line with previous (soft) trends.

We also believe the ongoing softness in manufacturing will take a bigger bite out of US growth than is commonly perceived, and this is the main driver of our below-consensus calls on GDP growth, inflation and Fed-hiking actions. Having said this, strength in Treasury bond markets today and in general over recent weeks is more due to Brexit worries than to US manufacturing softness. Over the longer term, however, we think the slower US growth will continue to be an issue for US financial markets, even after the current fixation on Brexit has faded from the headlines.