2015年07月07日時点

Foreign trade data for May were released this morning and showed deterioration in the US trade deficit, with exports dropping more than imports. Much of these declines marked a reversion to underlying trends. That is, due to a strike that hit the California ports of San Pedro and Long Beach earlier this year, both export and import volumes were overly depressed in February and March, then in April both made up for lost time, in effect, after the end of the strike. We then saw a move back toward underlying trends with the May trade data.

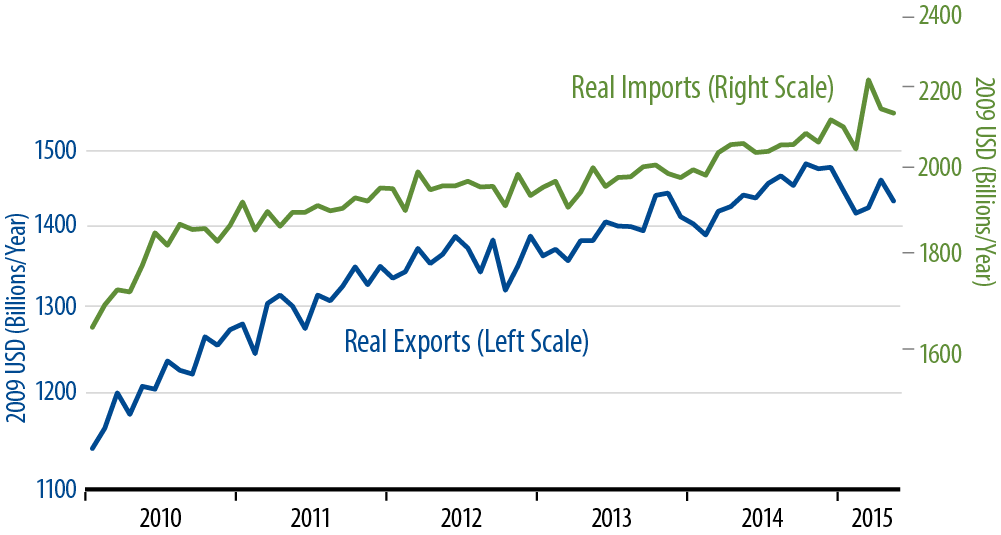

Unfortunately, those underlying trends are not favorable. As seen in the accompanying chart, exports have been trending lower since last October, and after the aforementioned strike effects over February–April, May export levels are right in line with on an ongoing downtrend. On the other side of the ledger, imports were on a steady uptrend last year, and after some jagged, strike-related interruptions of that trend over February–April, May import levels were right back on a rising trend line.

Falling exports and rising imports mean a steady rise in the trade deficit and, thus, a steady drag on US factory-sector production. As we have related before here, US factory-sector activity has flagged noticeably this year, driven by weakening in capital spending and exports. The recent data show both of those drags still in place, indicating, in turn, that the weakening trend in factory output is continuing as well.

Manufacturing is not a large enough sector to single-handedly pull the US into recession, but it is large enough that its current stall has imparted a noticeable hit to underlying GDP growth. At the start of the year, we were expecting growth in the 2.0%–2.5% range. The emerging softening in manufacturing has pushed underlying growth as much as a full percentage point lower.