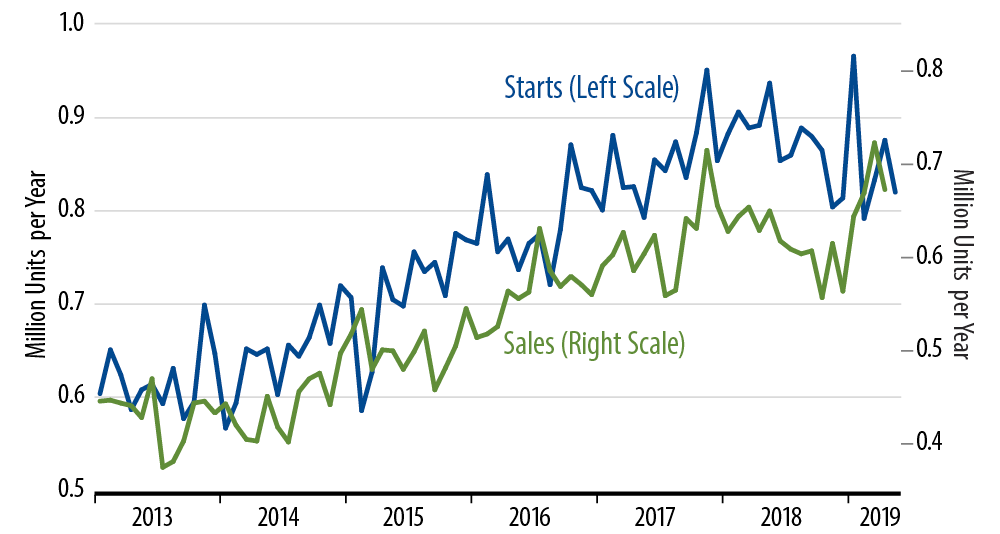

We haven’t covered the housing markets in these By The Numbers installments in a few months, but the picture there is pretty much the same as what we found it to be previously. Homebuilders got ahead of demand when they increased construction rates in 2016 and 2017, to the point that accumulated inventories of unsold new homes reached 7.4 months’ worth of sales late last year, an unsustainably high level of inventories.

In response, builders have been cutting back production since late-2017, but new-home sales declined as well early last year, so that inventories had continued to accumulate. Builders then employed discount pricing to move product, so new-home sales bounced in the early months of this year, allowing builders to start to address excess inventories. The combination of continued declines in (underlying levels of) single-family starts and discount-boosted sales has brought inventories down to 6 months’ sales in recent months.

However, discounted prices mean squeezed profit margins, and even 6 months’ worth of sales is an unsustainably high inventory level, so starts levels must go lower yet. This is all the more the case given that it looks as though builders moved to raise prices and repair margins in April, so that new-home sales are likely to pull back toward mid-2018 levels in months to come.

This is not a disaster scenario for the housing market, and we don’t think the current pace of decline in starts activity is steep enough to threaten recession. After all, starts were plunging at a 30% annual rate over 2005-2007, while the drop in the last year is only on the order of 10% or so. Also, housing demand is holding up dramatically better presently than was the case in 2005-2007. So, the bad news is that the recent declining trend in homebuilding has a ways to go yet. The good news is that that decline is still relatively orderly and mild.