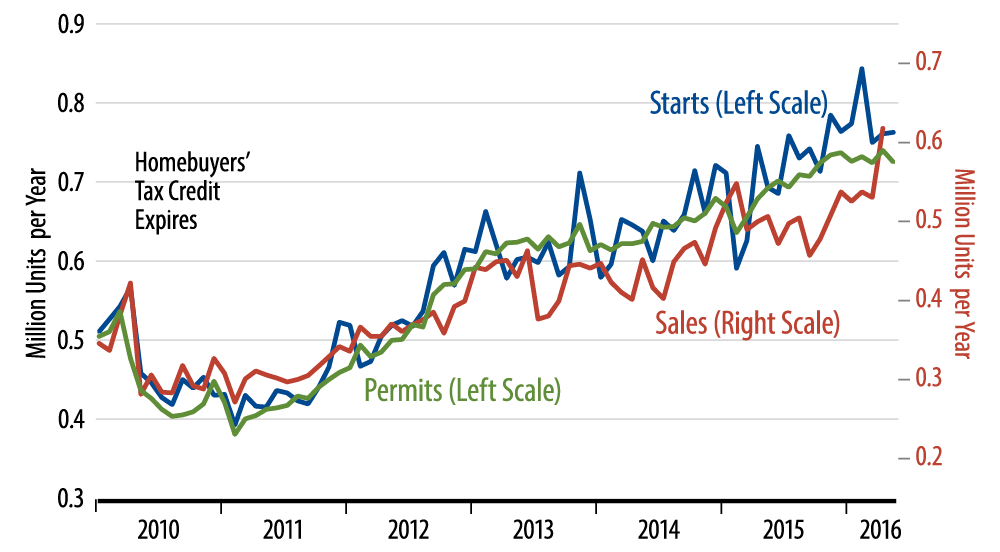

Housing starts were little changed in May, following March–April declines off a sharp February rise. The crucial single-family starts indicator performed similarly, up 0.3% in May, following changes of +1.5%, -11.1%, and +9.0% over the previous 3 months.

On net, single-family starts in May were lower than the levels of last November, as were starts in March and April. In fact, looking at starts in the accompanying chart (blue line), the only thing obstructing a conclusion that starts are now clearly on a flat or downward trend is that very high level of starts in February. In analyzing the April starts data in our May 17, 2016 installment of “By the Numbers,” we said that “a May print of 800,000 or less [for single-family starts] would support our contention that homebuilding is flattening out.” Well, May starts came in at 764,000.

What about the sharp April gain in new-home sales? Well, as commented in our May 24, 2016 installment, that was the first decent gain in new-home sales in over a year, and it barely brought sales to levels sufficient to sustain current housing starts levels. So, May and June sales levels will have to rise above April levels if homebuilding is to resume an uptrend that will give positive support to GDP growth.

Just to be clear, we are waxing bearish neither on the housing market in general nor on home prices. Rather, our focus is on homebuilding. The rising trend for single-family homebuilding over 2014–15 provided a boost of about 0.2 percentage points to GDP growth. Data for 5 months of the past 6 indicate that this uptrend is spent, and with it, the boost to growth. (Meanwhile, as recounted elsewhere, the US manufacturing sector has been a significant drag on GDP growth for at least a year now and will continue to be.)

Of course, that February surge in starts still clouds the picture. Evidence in the other direction continues to pile up, but the picture is not crystal clear as yet. Meanwhile, in multi-family housing, the picture is clearer. Multi-family homebuilding has fallen substantially (more than 10%) from highs achieved in the spring of 2015.