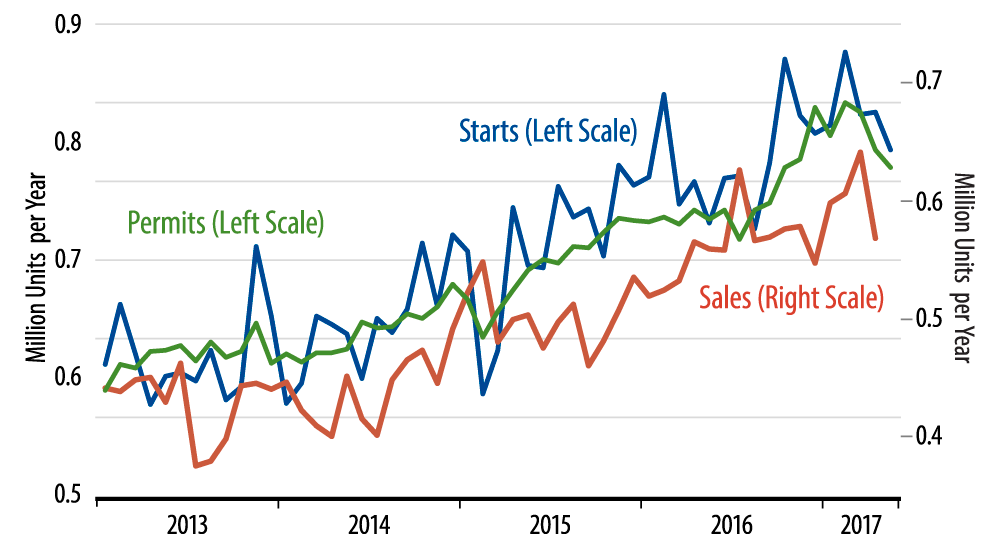

The backstory here is that homebuilding has been strong since last October, when starts jumped sharply. While a similar spike in starts in February 2016 was quickly reversed, the October spike was largely sustained for the next six months through April. The May decline announced today pulls starts levels below the prevailing range of recent months.

Our take had been that the late-2016 surge in starts got homebuilders ahead of their market. As you can see in the accompanying chart, sales of new homes never rose enough to validate the higher level of starts, and in accord with this, inventories of new homes have been on the rise ever since October. We take the recent declines in starts as an indication that homebuilders are trimming activity to get supply in better accord with demand and to head off accumulation of unwanted inventories.

Note that there hasn’t been any actual weakness in new-home sales recently. They merely hadn't increased in line with homebuilding activity. So, we are not looking for an ongoing declining trend in residential construction activity, just a reversal of the gains seen since October.

Residential construction has been one of the few segments of the economy boosting GDP growth over the last few quarters. That boost is unlikely to be sustained over the rest of the year.

Early this year, we upgraded our 2017 GDP forecast based on better news out of the manufacturing and homebuilding sectors. Both of those "rebounds" have faded in recent months, and it is now looking as though GDP growth will be sustained in the one-handle range over the rest of the year (though 2Q17 growth will likely be a bit better, as an offset of the especially soft 1Q17 print).