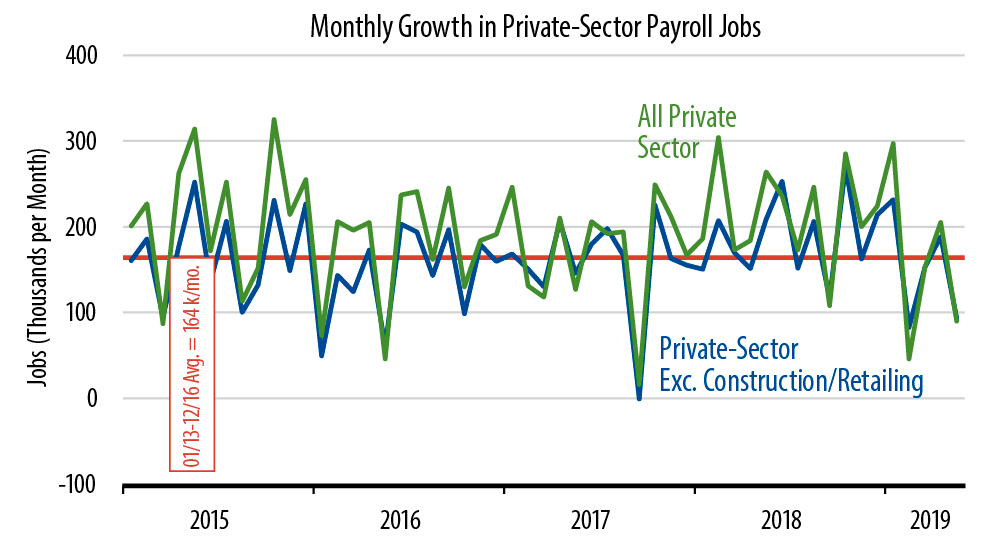

The net effect of all this news is displayed in the chart below. As always, job growth is volatile month to month, even when the most volatile sectors are abstracted from. Nevertheless, it is clear from the chart that job growth has generally slowed this year from the pace of 2018.

For the five months from January through May, our preferred jobs measure showed average growth of 150,000 per month, down from a 2018 average rate of 189,000 per month and from a 2013-16 average of 164,000 per month.

We said a month ago that the April jobs news elicited a sigh of relief from financial markets worried about slowing economic growth. Today’s data negates that relief.

We have been paying special attention to the manufacturing sector, which has been foundering in 2019 following two years of strong growth from late-2016 through late-2018. The May data showed further declines in both factory production workers and production hours. Since January, factory production jobs have declined by -24,000 or -0.3%, while production hours have declined by -1.3%. These data imply another weak industrial production number from the Fed next Friday.

While manufacturing has weakened lately, it is still not as soft as it was over 2015-16. Construction activity is a bit weaker this year than it was over 2015-16, while the service sectors are about the same. Average GDP growth over 2015-16 was around 1.5%. On net, recent data don’t threaten recession. However, they do indicate noticeably slower GDP growth than we saw over 2017-18.

A month ago, we stated a GDP forecast of 2.0%-2.25%. The downward personal income revisions and related retail softness discussed last week served to trim that call to the 1.75%-2.00% range, and today’s data are roughly consistent with that. Again, no recession, but likely enough slowing to nudge the Fed toward easing moves.