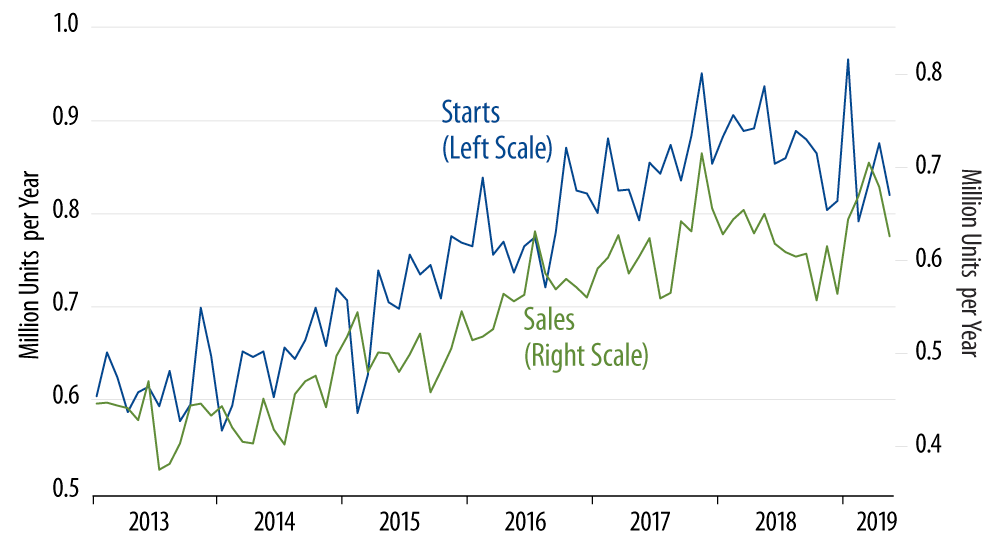

In last week’s installment we stated that homebuilding was on an orderly downtrend, with starts trending lower but at a leisurely pace, while sales levels were starting to head lower after a bout of discount prices had pulled sales to unsustainably high levels early this year. We thought inventories of unsold new homes were still relatively high and that starts would have to head still lower in order to fully address the inventory overhang.

Today’s data are more or less in line with that outlook. As daunting as a -7.8% monthly swing might sound, you can see in the chart that that decline still leaves May new-home sales levels somewhat above the levels of late-2018.

Again, the downtrends in both these series remain orderly. We still believe housing starts will continue to work lower from here, but the homebuilding market is not giving off the signs of severe weakness that would suggest a recession in the offing.

Another promising element of the new-home sales data is that sales are holding up just fine in the South, where 50% of homebuilding occurs. It appears that the home inventory overhang we have talked about is centered in the Northeast and Midwest, perhaps also in the West. It is in those regions that sales and starts have pulled lower most obviously over the last year. With the bedrock of the housing industry (the South) holding up relatively well, that is another reason not to expect a more serious rate of decline.

Finally, inventories of unsold new homes did tick up in May, after declining earlier this year. For the nation as a whole, new-home inventories amount to 6.4 months’ worth of sales. This is unsustainably high, and this inventory overhang is the reason we believe housing starts levels must work lower still over the next few months before they can stabilize.