2015年06月05日時点

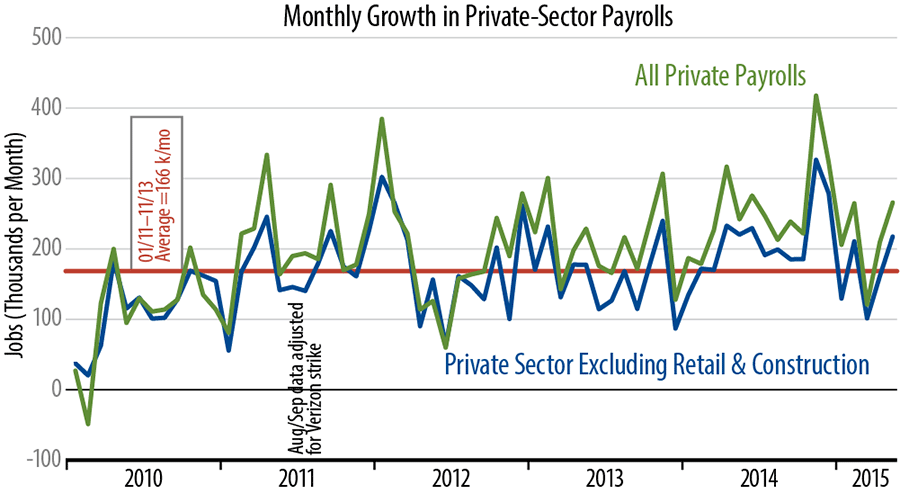

May payrolls came in above expectations, following four months of generally disappointing news. Private-sector payrolls rose 262,000, along with a +16,000 revision to previous months, and our “core” jobs measure (excluding retailing and construction) rose 214,000, compared to average gains of 166,000 per month over the last four years.

The accompanying chart tells the story. May job gains were above-average, following generally below-average gains earlier in the year, but also following a job surge in late-2014. We always caution not to get too excited about any one number—neither upward nor downward—and that advice holds here. Following a very disappointing first quarter economic performance, we have seen better news lately, but we have yet to see whether the recent news is the new norm, or a brief, upward fluctuation (comparable to that of late-2014).

Last month in this column, we focused on payrolls and production hours within manufacturing. Weakening there since last November had been the primary cause of very weak 1Q15 GDP, and factory payrolls weakened again in April. Well, here, too, the May data saw improvement, with both factory jobs and production hours rising. Here too, though, the May gains are less than decisive, leaving May production hour levels still well below the November levels.

It is understandable that the financial media and consensus analysts are jumping on today’s data as an “all clear” signal for the economy going forward. While we would agree that today’s data are better than we have seen, we think that consensus “rush” is premature. From plunging drill rig activity, softening capital spending and exports to ho-hum consumer spending, there was more holding the economy back in first quarter than just bad weather. And with the economic data as volatile as they are, it takes more than one month of better data to dispel the slower growth trends that we have seen so far this year. In sum, so far, so good, but don’t crack open the champagne just yet.