"It's time to ask yourself, what do you believe?" (Indiana Jones and the Last Crusade 1989)

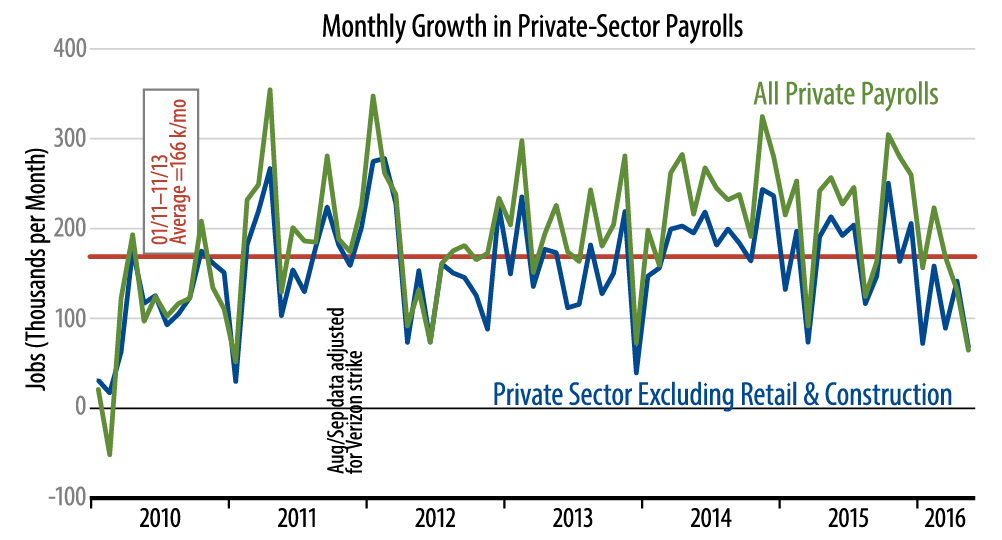

May payroll jobs came in with a thud today. Headline private-sector payroll jobs rose by only 25,000 in May. Even adding back losses due to the Verizon strike, the gain was only 63,000, and that was almost fully offset by -58,000 of revisions to March and April data. The core jobs measure we track—private-sector jobs less uber-volatile retailing and construction—was up 67,000 allowing for the Verizon strike, with a -49,000 offset from revisions of previous data.

Any way you slice it, this was a weak report. More to the point, as we have been remarking for the last few months, job growth has actually been markedly slower throughout 2016 to date. The accompanying chart establishes this point clearly.

Slowing job growth goes hand in glove with GDP data that will likely show 4-quarter growth of only 1.5% through 2Q16. For 120 years through 2005, the US economy grew at an average rate of 3.25% per year.

Since the peak of the last expansion, growth has been 1.4%, and even during the expansion phase since 2Q09, average growth has been only 2.1%. Now, growth has slowed still further.

Can the Federal Reserve (Fed) really sustain an increase in yields in this environment? Many within the Fed and elsewhere have claimed that 1.5% GDP growth and 100,000 to 150,000 per month job growth is all the US economy is currently capable of. Will the Fed really ratify these claims and resume rate hikes at current growth rates? Even if the Fed remains intent on merely "normalizing" yields, it will still have to come to grips with the question of what exactly a "normal" level of yields is when trend growth is 2 percentage points below historical norms and when inflation remains stubbornly low.

Good questions one and all. For now, it looks as though a slower growth environment is firmly ensconced, and the Fed, like Indiana Jones, must ask itself what it really believes.