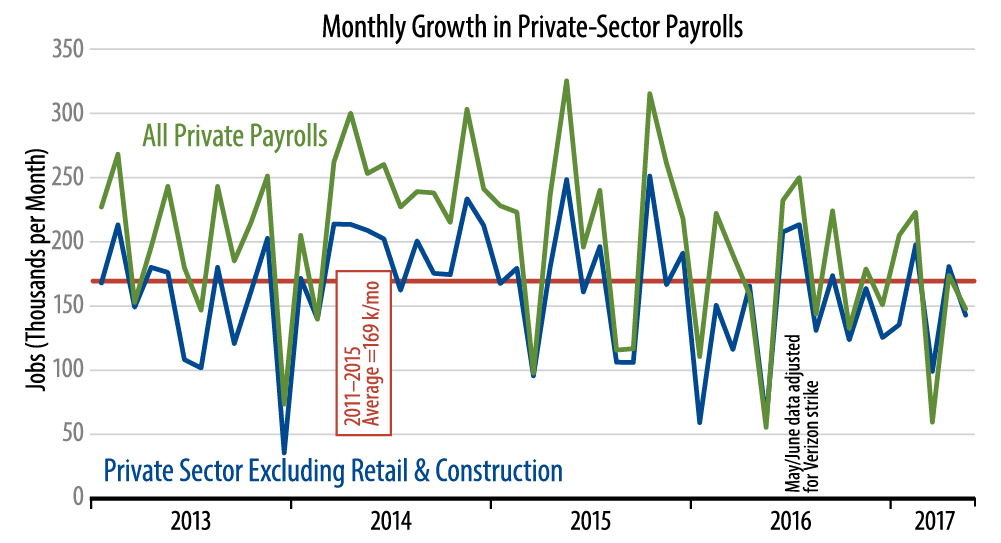

We focus on the latter measure because of the short-run extreme volatility that construction and retailing jobs show, and that goes for revisions as well. When all is said and done, the job gains of May—and, indeed, for the last 10 months as a whole—show growth to be decent, but at a much slower pace than the economy saw over 2010 through 2015. This shows up clearly in the chart.

Market and media buzz today is likely to be very disappointed with today’s numbers. Street forecasts were clustered around 200,000, and yesterday’s ADP jobs estimate reported gains of over 250,000. The actual data were way below those guesstimates and estimates, but, again, they were of a piece with what we have seen over the past 10 months.

There is nothing in these data suggestive of actual economic weakness. The disappointment is that the market consensus has been looking for a growth acceleration this year, and the actual data have stubbornly refused to comply.

In line with this theme, the much vaunted acceleration in wage gains has also failed to “take wing.” With modest May gains announced this morning, hourly wages look to be growing recently at an underlying rate of about 2.4%—not horrible, but about half a percentage point slower than what we were seeing this time a year ago.

While we raised our GDP growth outlook early this year to the 2.0%–2.5% range, that remained lower than the market consensus. It is starting to look as though even our expectation was a bit too optimistic. Again, there is no actual weakness in the recent data, but there is no sign of the widely anticipated growth acceleration either.