Retail sales grew nicely in May, with headline sales up 0.5% and April sales revised up a bit. Our control sales measure, excluding vehicles, gasoline and building materials but including restaurants, was up 0.5%, and the April level was revised upward by 0.2%.

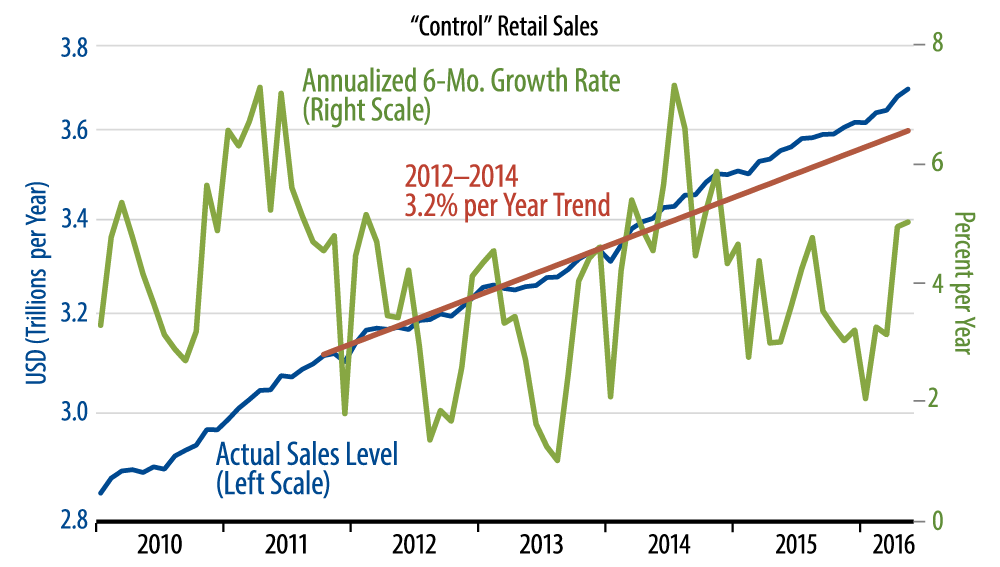

So, the May sales gains were not as strong as those of April, but they were a nice follow-through, given how strong April sales were. As seen in the accompanying chart, control sales moved further above 2012–14 trends over the last 2 months after having first moved above trend about a year ago (and then languishing in late-2015).

Sales gains continued strong at nonstore (online) retailers and there were also good gains at bookstores, sporting goods stores and grocery stores. Meanwhile, sales continued sluggish at department stores, apparel stores and car dealers, and sales have weakened markedly in the last few months at building material stores.

The good sales growth in April and May should dampen any recession fears that have been surfacing recently. It could also bring July back in play for a Fed rate hike, provided next month’s jobs report is markedly better than what we saw this month. However, it doesn’t change our forecast of soft underlying GDP growth, 1.5%, rather than the 2.0%–2.5% the Fed and many market mavens are calling for.

Capital spending and export trends continue soft. With most of the goods purchased by consumers at retail stores being imported, we see nothing across the range of data suggesting better growth for the US manufacturing sector. And soft factory growth is the baseline for our slow-growth outlook.

So, again, the retail report should stem downside fears, but it is probably not a harbinger of upside risks for US growth.