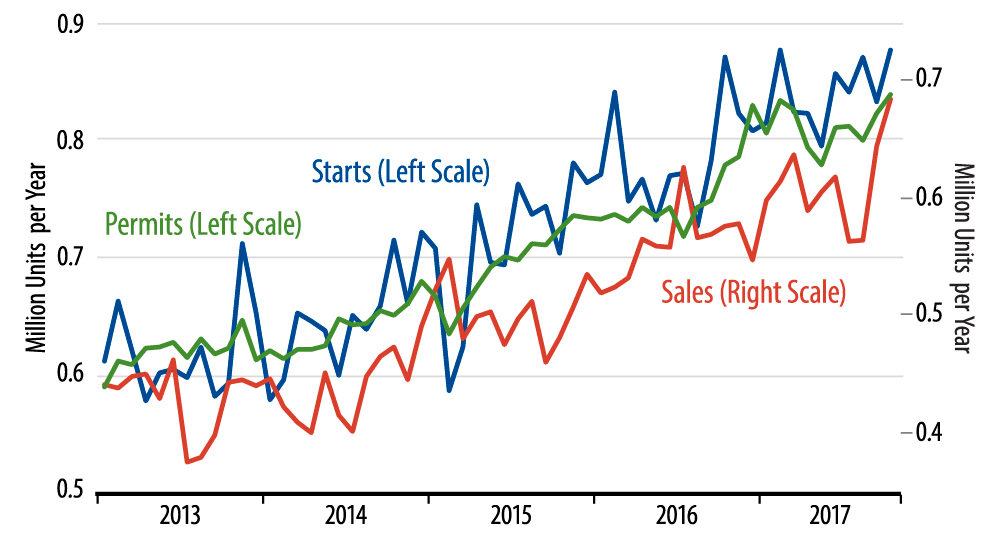

In other words, the last two months’ home sales data do not point to any net improvement in housing demand, but merely a reversal of hurricane-induced weakness. On net, new-home sales have remained flat for most of the past year, alongside similarly flat levels of home construction. As seen in the accompanying chart, housing starts also saw a bounce in October, and this bounce also merely served to offset hurricane-induced softness in starts in previous months.

The recent swings in housing starts have not been as sharp as those seen for new-home sales, but the contours are in line. Also supporting our contention here is the fact that most of the recent swings in both housing starts and new-home sales occurred in the South, exactly where the hurricane effects were felt.

If we are right, we will see declines in November in both single-family housing starts and new-home sales. That is, if the elevated levels of starts and sales in October are merely a catch-up of hurricane-delayed activity, then both starts and sales will revert to their “ongoing” levels in November or December; these levels will be announced in December and January.

As before, we are not claiming that there is any actual weakness in housing. Our contention is that the market has topped out over the last year and will remain flat going forward, such that homebuilding will not be a source of any boost to GDP growth.

Consistent with this contention is the fact that inventories of new homes have continued to increase across the last four months. New-home supply remains a bit ahead of demand, and our guess is that homebuilders will delay pushing construction levels higher until they see a net advance in new-home demand.