2015年06月25日時点

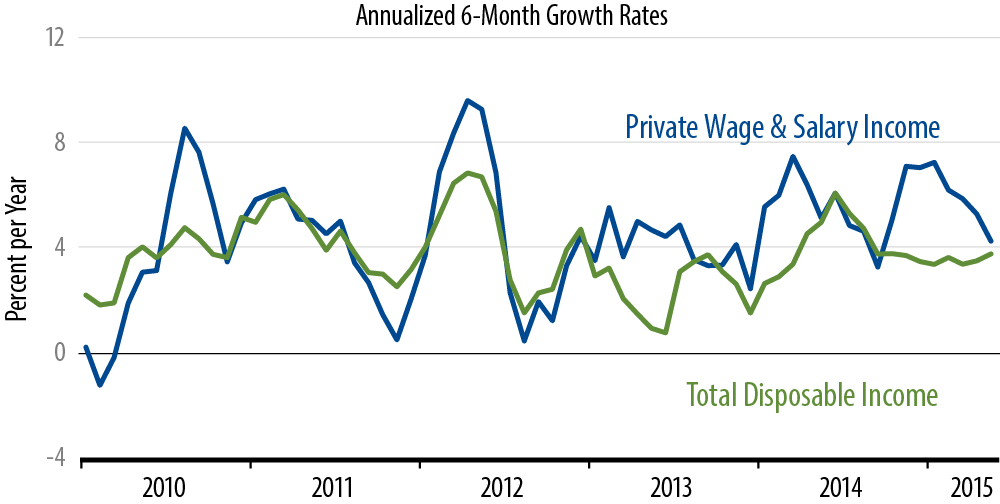

We learned today that most measures of personal income showed gains of 0.5% in May, reflecting the better payroll job gains for May reported three weeks ago. What we find most interesting is that the May gains fail to make much of a dent in sluggish underlying income growth trends. As seen in the accompanying chart, nominal disposable incomes have grown at only a 3.8% rate since March 2014.1

To hear most analysts tell it, job growth has been buoyant since early-2014. Since then, wage income has picked up, but not total disposable incomes, and the growth in total incomes is only about consistent with the growth in consumer spending seen in that same timeframe.

Why didn’t faster job growth push faster growth in total income? First, much of the job growth was driven by individuals re-entering the workforce once extended unemployment benefits expired in December 2013, and second, tax burdens have been steadily rising.

A January 2015 National Bureau of Economic Research study2 found that 1.8 million new jobs last year can be traced to the expiration of benefits. For those workers, gains in wage income were partially offset by the loss of benefits, so the wage income growth numbers are misleading. Meanwhile, effective individual tax rates have risen from 9.6% at the trough of the recession to 12.3% in May, almost back to the pre-recession norms of 12.5%.

The bottom line is that despite better job growth, personal incomes are not rising fast enough to drive any sustained acceleration in consumer spending. Meanwhile, as seen in the blue line in the chart, even wage income growth has been slowing lately. The nice income gains of May are balanced by more sluggish gains over the previous five months.