2015年05月13日時点

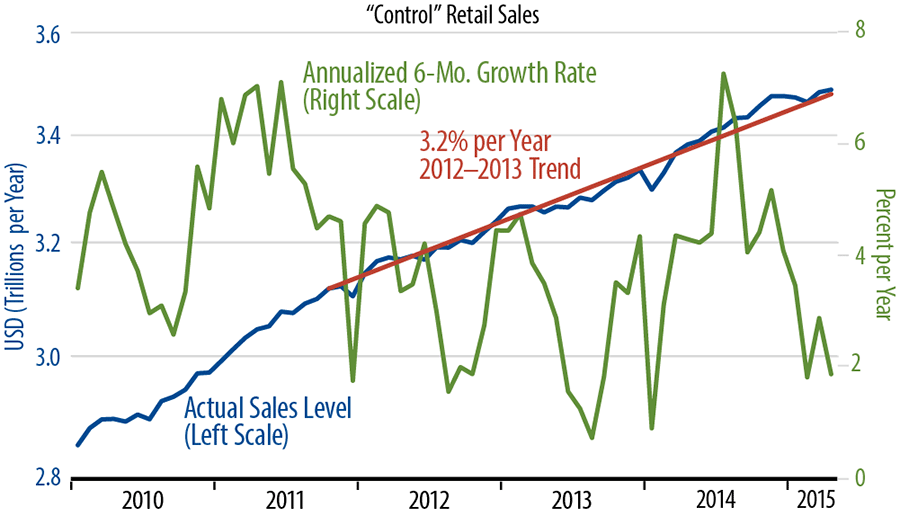

April retail sales came in weak this morning, with headline sales flat in April following a 1.1% gain in March, revised up from 0.9% in the initial report last month and following a 0.6% decline in February. The core sales measure we track (see accompanying chart) was up a scant 0.1% in April, with the March gain revised from 0.4% to 0.5%, and February revised from -0.2% to -0.3%.

The trend of economic data over the past six weeks has been unrelentingly soft, and today’s news was more of the same. As seen in the chart, “control” sales are right on the mediocre trend line they have followed for the last four years, contrary to widespread hopes that better job growth and lower gas prices would spur an acceleration in consumer spending.

Note also that the “control” measure followed here is slightly different from that followed by most analysts. The others exclude restaurant sales from their “control” measure, because the U.S. Department of Commerce now includes restaurant spending in the services component of GDP data rather than the goods sector (where other retail spending goes). We include restaurant sales in our “control” measure, because these have always been part of the retail report. Anyway, restaurant sales have been one of the few bright spots for retailing lately, so the retail trends reported here are drab despite including stronger restaurant data.

Note finally that consumers are not just suddenly reeling after a strong spending spurt. Again, recent data merely bring sales back to the trends in place prior to the October/November spike of late-2014. If severe early-2015 weather were the factor holding sales down, the softness in January and February 2015 would have been followed by overly strong gains in March and April, as happened a year ago. That this didn’t happen this year is a clear indication that it was the stronger October/November gains that were the aberration, not the recent data.

On net, we have seen steady, drab retail sales growth across the last six months, opposite clear slowings in exports and capital spending and, through April at least, a net slowing in US economic growth.