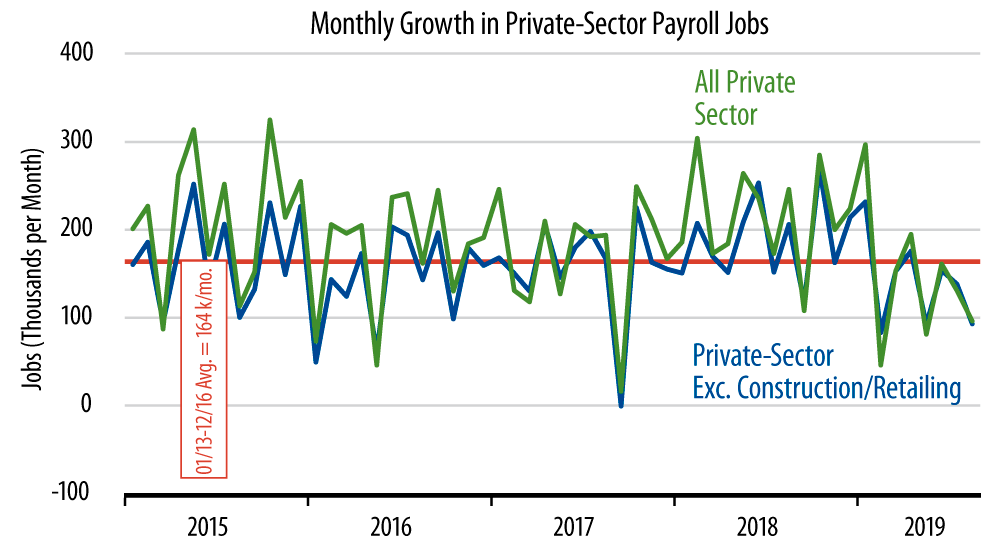

As you can see in the accompanying chart, the August job gains were down some from the previous two months’ gains and below the average growth pace of the previous few years, but were about in line with what we have been seeing over the course of 2019.

We were hoping for some clarity in the job gains, a number either weak enough to credit the recession fears or strong enough to dispel them. Instead, we got something in the middle. Coming in, we all knew that US economic growth had downshifted in 2019 from the elevated pace of 2017-18. Today’s data merely confirm that. At the same time, there is no apparent ongoing slide to recession-like labor market performance. Indeed, many analysts would contend that current job growth rates still match or exceed the pace consistent with full-employment growth.

An encouraging sign in today’s report is that manufacturing payrolls continue to show signs of stabilization following a 6-month swoon early in 2019. Thus, factory production jobs and total production hours worked both bounced in August. Indeed, production jobs have risen (though slightly) in each of the last three months, after declining over the previous five.

Many analysts are bemoaning factory weakness as if it were a recent development, thanks to the factory Institute for Supply Management (ISM) index dropping below 50% in the latest report. However, "hard data" on manufacturing have been in downtrend mode since the fall of 2018. We have always been skeptical in general of the "soft data" indices such as the ISM, and lately these appear to be lagging indicators. Factory orders and production data have been showing signs of stabilization for a couple months now, and the manufacturing information in today’s payroll release continue that skein.

In fact, as much as we might bemoan the presence of the trade wars and have caution over their possible effects, it is hard to find any real evidence of them having an actual effect on the economic data. Again, the manufacturing data have seen at least a faint bounce in recent months, the recent US foreign trade data have actually shown improvement relative to previous trends, and capital spending, which had been soft for almost a year now, is also showing a mild bounce recently.

It is one thing to say that growth would be stronger were the trade wars not part of the picture. It is something else entirely to claim or fear that they will drive a recession. It is hard to see any sign of the latter in the recent data.