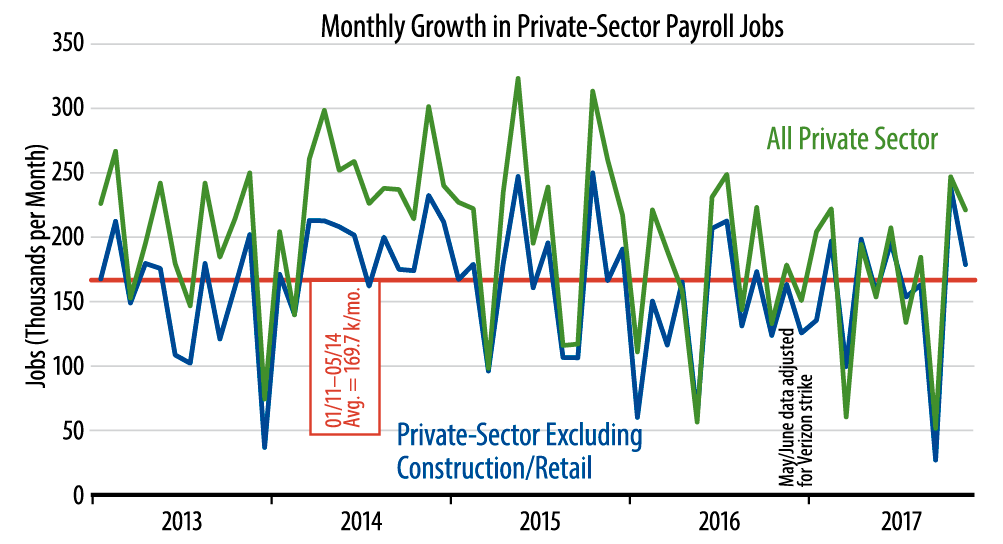

October’s job gains were larger than what we saw for November, but that was because the October gains were mostly a snapback from hurricane-depressed September job levels. Indeed, the October gains did not fully offset the below-trend experience of September, so some of the November gains should also be viewed as hurricane-snapback.

Average the last three months together—both hurricane-depressed and hurricane-snapback—and our core measure shows growth of 148,000 jobs per month since August. This is actually below the 170,000 per month average seen in recent years.

Once again, our core jobs measure abstracts from construction and retailing, because of the particularly high short-term volatility these sectors show, especially around this time of year. Construction job growth in November was steady at +24,000, with gains there in recent months right on trend. Retail jobs rose by 29,000. While this is a pick-up from the declining job trend retail had shown through the first eight months of the year, one should keep in mind that November marks the start of the Christmas hiring season, so, again, these sectors are subject to seasonal distortion.

Today’s report was disappointing to Wall Street in that hourly wages rose only 0.2%, with a 0.15% downward revision to October. On net, the 12-month growth rates in hourly wages for all workers rose “only” 2.5% through November, below expectations (hopes?). We actually prefer the older measure that covers average hourly wages for nonsupervisory workers (those workers who are actually paid by the hour, rather than drawing a weekly or monthly salary). The latter measure was also up 0.2% in November, with a 0.15% downward revision to October, but its 12-month growth rate is a mere 2.3% and has been decelerating steadily over the past two years.