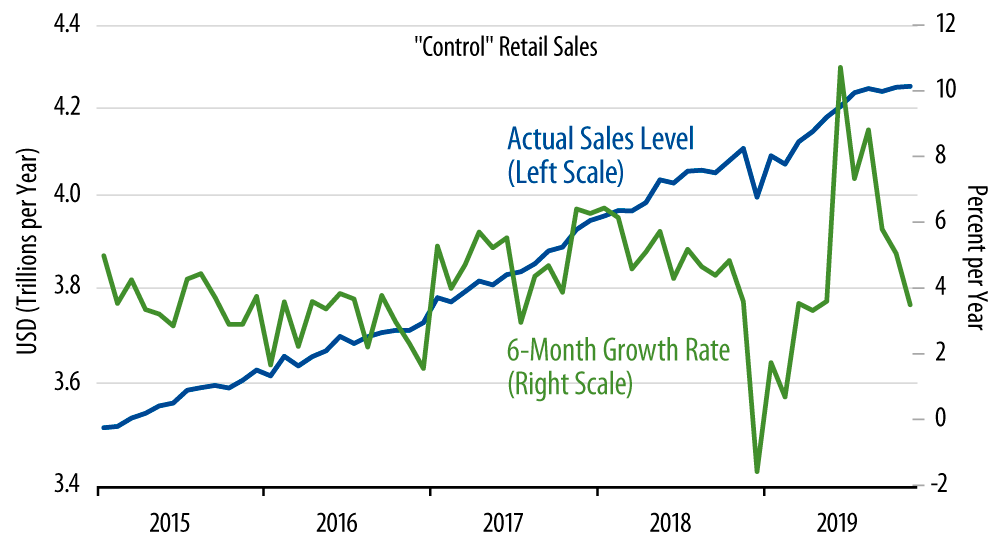

The control sales data are summarized in the chart. As you can see, the tepid November sales gains came on the heels of similarly tepid gains in recent months, so that the very recent retail sales data suggest a slowdown in the rate of growth of consumer spending on merchandise.

To flesh out the context here, we’ll point out first that services spending, which accounts for about 60% of total consumer spending, shows no such slowing. Second, the slower recent growth in retail sales comes on the heels of a very strong run of retail sales releases over February through August, so that the six-month growth rate in control sales still comes in at a healthy 3.5% growth rate, with the 12-month growth rate at 3.6%. Finally, personal income growth has remained healthy through October, and last week’s November jobs report indicates good income growth last month as well.

Perhaps the consumer is just catching their breath after a strong run in mid-year. Then again, perhaps it is the government statisticians that are catching their collective breath. That is, one must always be suspicious about seasonal adjustments at this time of year.

Last month, we mentioned that the seasonal adjustments applied to the October data were much harsher than those applied to October 2018 data, with seasonal adjustment taking 5.4% out of unadjusted control sales growth in October 2019, compared to 4.5% in October 2018. That cannot be said with respect to November, as seasonal adjustment took 6.0% out of November 2019 unadjusted sales growth, compared to a 7.1% subtraction in November 2018.

However, besides monthly effects, the seasonal adjustments applied to November also include adjustments for the number of weekday shopping days and for the earliness or lateness of Thanksgiving. (This year, Thanksgiving occurred as late in the month as it could.) So, no one knows for sure whether the 1.1% "boost" in seasonal adjustments this year over last is really sufficient to cover the difference in "timing" of the successive Novembers.

Sorry if we got lost in the weeds here. The point is that at this time of the year, seasonal adjustments are especially prone to uncertainty. (They will be through the February data.)

Beneath all the noise, retail sales trends are not weak per se, just softer than the buoyant growth seen in mid-year. As you can see in the chart, the retail sales data have shown all sorts of zigs and zags over the last 15 months, only to eventually return to a stable trend. Despite the apparent softness in very recent sales reports, our guess is that consumer spending growth is actually chugging along steadily.