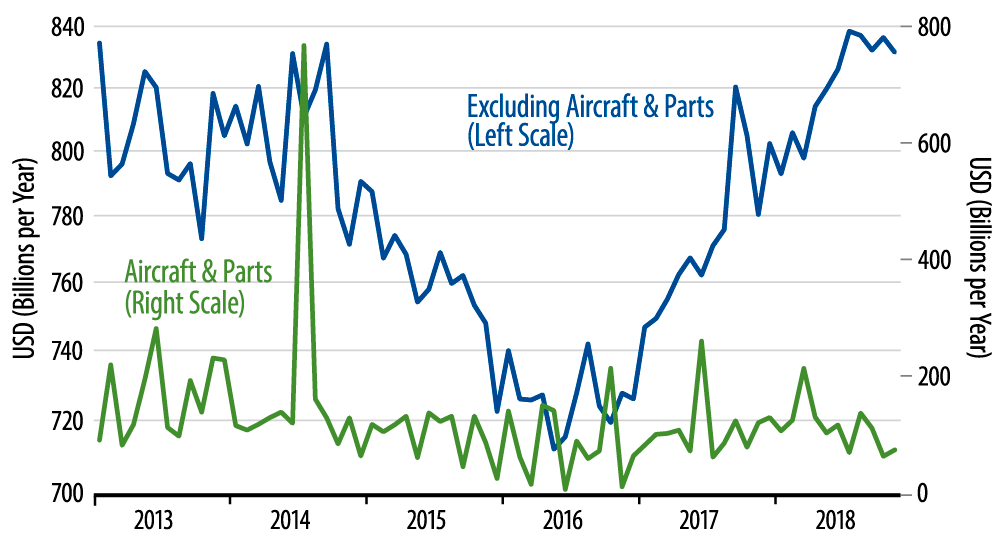

Similarly, new orders for capital equipment continued soft, with orders for capital equipment excluding aircraft declining 0.6%, only partially offset by a +0.5% revision to October. As seen in the chart, capital goods orders have been trending lower for the last four months, and the November news is just a continuation of that trend.

Also, while orders for aircraft and parts increased 17.5% in November, even that gain is only chump change compared to a 54.5% cumulative decline over August and September. All in all, aircraft activity is flat at best, and CAPEX activity, which should be strengthening in the wake of corporate tax reform, has hit a speed bump, after strong growth over the preceding two years.

We’ve been emphasizing in these posts that it is manufacturing that has powered what pick-up the US economy has seen over the last two years, that that pick-up has been driven by foreign trade and capital spending, and that exports, capital spending, and factory activity in general have all been softening in recent months. Along with declines in homebuilding, we believe this concerted softening is enough to pull aggregate US growth down to the 2% range from the 2.8% enjoyed over the last two years. Today’s durable goods news is right in line with this outlook.