~William Shakespeare

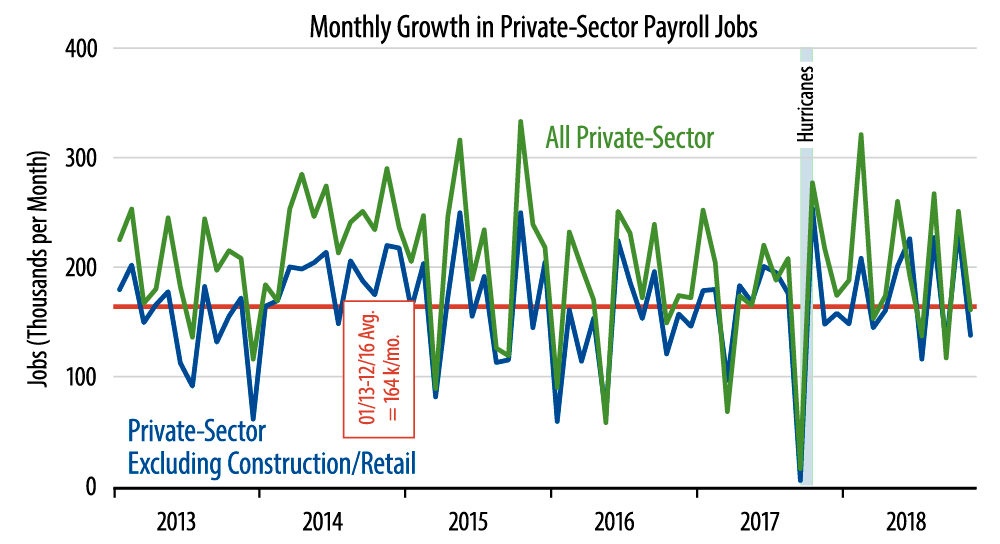

Private-sector payroll jobs grew by 161,000 in November, with October’s job level revised up by a scant 1,000. For our preferred measure, private-sector jobs excluding construction and retailing, the gain was 138,000, with a +16,000 revision to October. That compares to a recent years’ average gain of 164,000 per month. This news fell short of market expectations.

A month ago, in our November 9 By The Numbers installment, we guessed that economic growth would slow, inflation would stay low, and the Fed would moderate its schedule of rate hikes for 2019. Those were outlandish expectations then, but reality has swung in the past month to where this has become a "consensus" outlook. Sentiment has now swung so sharply that a consensus that saw only the positive in the data just a month ago now sees only the negative.

In fact, recent economic data are only slightly softer than prior data, but sentiment now reflects worry about recession: doom and gloom from euphoria just a month ago. Look at the accompanying chart. Yes, the November data were softer than the October data, but the chart depicts these swings as nothing more than standard, random (?) fluctuations that have occurred repeatedly over the past few years. Talk about "sound and fury."

Our preferred jobs measure excludes construction and retailing because of the extreme seasonal volatility these sectors display over the winter months, even in seasonally adjusted data. We believe our measure is to be...preferred at least for another three months. Still, even our measure shows its share of month-to-month random chop.

We do still believe growth will be slower going forward than it has been over the last year or so. However, at the same time, very recent economic data have not shown actual weakness. They have merely failed to match the market’s expectations of continued buoyant growth.