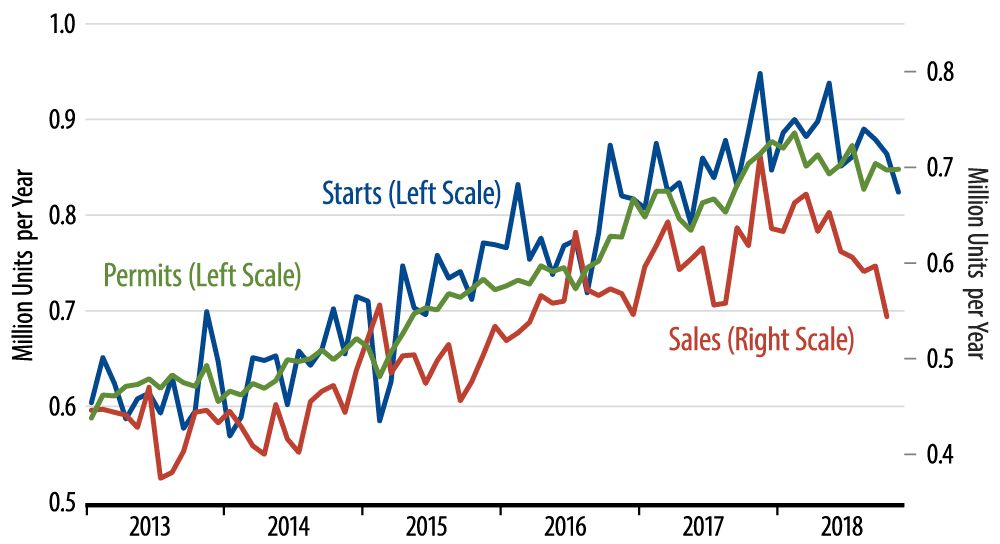

Earlier this month, we got news that single-family housing starts dropped again in November, down 4.6%. This decline was likely overstated by the effects of wildfires in California. (Single-family starts in the West declined 24.4% in November.) Nevertheless, starts had already been on a downtrend throughout the year, which is evident in every region of the country. So, the wildfires may have exaggerated softness in homebuilding, but they were not the driver.

The chart shows single-family starts and permits nationwide through November, along with new-home sales through October. You can see the clear downtrends throughout 2018 in all these measures. In fact, sales have been lagging starts for the past five years, so that through October, inventories of unsold new homes had risen to 7.4 months’ worth of sales, way above a normal level of around 4 months’ worth of sales.

New-home sales had dropped so much through October that we expected some bounce in November, as builders’ sales promotions (price declines) started to kick in. We’ll see whether that shows up in the data when the government shutdown is finally over.

What’s driving the softer new-home market? Higher mortgage interest rates haven’t helped, but deeper factors are also in play. Labor force participation rates among 25- to 34-year-olds have bounced a bit in the last year, but they remain very low, and this cohort accounts for the bulk of first-time homebuyers. Meanwhile, mortgage lending standards remain much tighter than they were a decade ago, and the need for a 20% down payment is a major sticking point.

Our sense is that the homebuilding sector has been in "failure-to-launch" mode throughout the current expansion and that the recent pullback is just an inevitable correction after four years of increasing homebuilding activity. The good news is that we don’t foresee a housing collapse that could derail the aggregate economy. Still, homebuilding is not likely to provide any boost to economic growth next year.

Thank you for your support of By The Numbers in 2018. Our best wishes for a successful 2019.