2014年12月23日時点

In a pre-holiday extravaganza, four major economic reports were released today. We’ll focus here on new-home sales, but we’ll also provide some coverage of the other news: 3Q14 GDP, November personal income, and November durable goods orders.

On net, the news today was a push, with GDP revised strongly upward to 5.0% real growth and with personal income and consumer spending up strongly for November, but with durables and capital goods orders down, and new-home sales and sales prices down. Prior to today, the economic news this month had all been positive, so one could say today’s mixed bag was an inevitable pause. Others have looked upon the softness in CAPEX as a reflection of the ill effects of falling oil prices.

Certainly, consumer spending data have looked better lately, but that new-found consumer buoyancy has not transferred over to an appetite for housing. New-home sales levels remain in the flat-to-down range that has held for almost two years, and, again, the softness in sales looks to be seeping into home sales prices, which have been flat on net for the last six months.

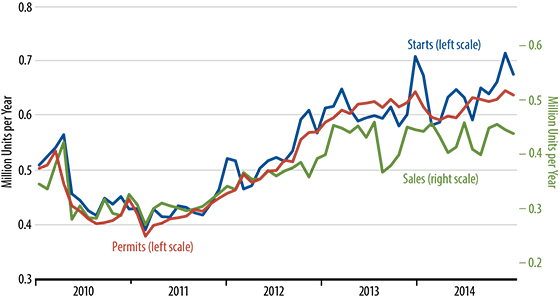

As seen in the accompanying chart and as commented upon here last week, builders boosted housing starts levels in October and November, but home sales have not followed through, resulting in increases in homebuilders’ inventories. (And builders have also kept permits levels on a flat trend.) Our guess is that the recent housing-starts bulge will be reversed in months to come, just as was the case with a similar bulge a year ago.

Meanwhile, capital goods orders have been flat to down for the last five months. However, those declines come on the heels of an extraordinarily strong gain in June, so it is hard to tell whether CAPEX activity is really weakening or merely consolidating after an early-summer spike.

The consumer gains have been more clear-cut, wide-ranging, and impressive. Basically, the strong 2Q14 and 3Q14 GDP data average out an exceedingly weak 1Q14 print. In order for 3- and 4-handle GDP numbers to be a trend, rather than a one-time bounce, it will take continued strength in consumer spending plus strong growth in CAPEX and housing. The evidence is mixed as to whether the 2015 economy will achieve this parlay.

Happy holidays to all our readers and best wishes for a successful 2015.