These November data are the mirror image of what we saw a month ago, when headline sales gains were strong, core sales were softer, and both measures were revised downward. A month ago, we remarked that September and October news erased most of the signs of better retail sales growth that had arisen in the May and July sales data. Today’s renewed strong gains, then, put a better spin on the consumer outlook.

Then again, we saw a parallel bounce in retail sales in November 2017, only for underlying sales to go flat over the following three months. Indeed, a number of retail sectors showed November swings that echoed the gains seen 12 months ago. For example, online (nonstore) retailers have seen steady, robust sales gains averaging 0.8% per month over the last three years. In November 2017, however, they saw an exceptionally robust 3.2% gain, only for sales to pull back to the 0.8% trend in subsequent months.

Nonstore retailers are presently estimated to have seen a 2.3% sales gain in November 2018. We heard similar echoes of the November 2017 strength at furniture and book/sporting stores. It will be interesting to see whether any of these outsized gains hold up or prove to be one-time holiday shopping spurts much like we saw in 2017.

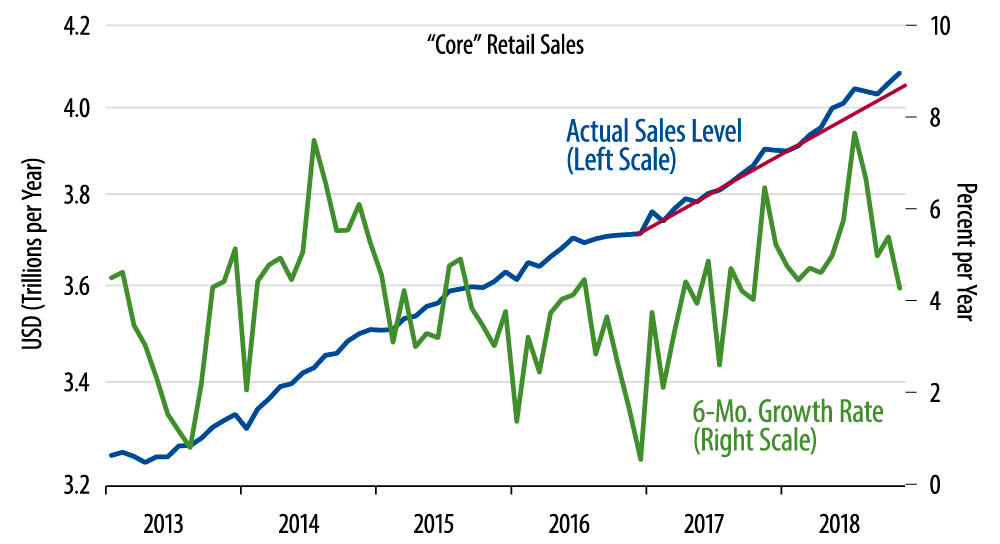

It could be that the November gains will be sustained and that consumers are embarking on a sustained spending spree, but we don’t think this is likely. Again, the November 2018 sales gains are redolent of similar bounces in November 2017, May 2018, and July 2018 that were subsequently reversed (see chart). Also, the latest data from the Commerce Department show a modest but noticeable slowing in income growth over the last six months, which argues against an acceleration in consumer spending presently. As always, time will tell.