2015年12月04日時点

Employment data showed decent growth in November, with private-sector jobs up 197,000 from October and substantial upward revisions to previous months. Household employment rose 244,000, following a 320,000 October gain, but these followed a September decline of 204,000.

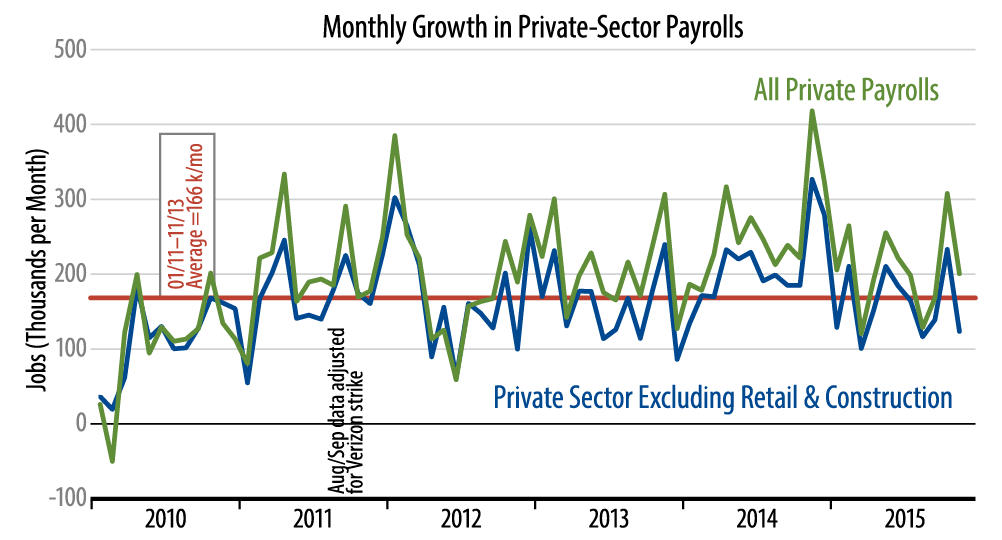

Once again, the gains were decent, following a strong October print, but we can’t wax as effusively on the release as the Wall Street consensus seems to be doing. As seen in the accompanying chart, the November gains are actually a bit below the average of the last five years. Also, much of the strength occurred in construction and retailing, which tend to be quite volatile from month to month. With homebuilding on the rise for now, there is reason to credit the construction gains. However, with retail sales soggy the last few months and early reports on Christmas sales disappointing, the retail job gains are more suspect.

Last, there is the issue of a substantial slowing this year in household jobs data. Though household jobs data did show good gains in October and November, those do not come close to fully offsetting the much weaker gains in household jobs seen earlier this year. Both payroll and household jobs showed average monthly gains of around 260,000 in 2014. Through the first 11 months of 2015, payroll job growth has slowed somewhat to 210,000 per month, but household jobs have slowed more substantially, to only 146,000 per month. No, the economy isn’t tanking, but only in a dumbed-down world would recent jobs data be seen as robust.

Meanwhile, the factory sector has been a focus of ours, and today’s data there were downbeat. Factory production jobs and production hours both declined slightly in November. This was a move downward from the bounce these indicators showed in October, thus a resumption of the downtrend seen through the first 9 months of the year. Declining October exports (also announced today) were a further indication of ongoing softness in US manufacturing. We believe the softness in US manufacturing will become a more noticeable drag on US growth in 2016, when the upturn in homebuilding is likely to top out.