It’s tough to write a piece called By the Numbers when there are no numbers coming out, at least not from government agencies. Since the federal government partially shut down two weeks ago, Commerce Department agencies such as the Bureau of Economic Analysis and the Census Bureau have ceased disseminating economic data. For some reason, however, the Bureau of Labor Statistics within the Labor Department has not been affected by the shutdown, so we did get a jobs report this morning (and will get Consumer Price Index and Producer Price Index data later this month, even if the shutdown continues).

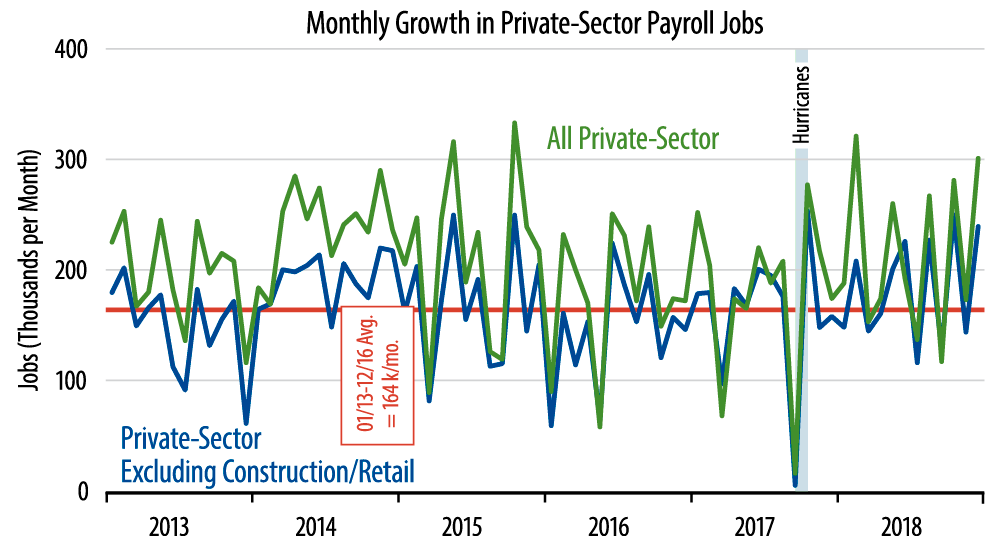

That (welcome) data showed private-sector payrolls up by 301,000 in December, on top of a whopping +42,000 revision to the November payroll level. Even our preferred jobs measure, private-sector jobs excluding construction and retailing, added 239,000 jobs in December, on top of a +22,000 revision to November, which compares favorably to a 164,000 per month trend for this series over most of the past five years.

For most of the past year, we have commented that job growth over 2017-18 was actually slower than what we had seen in 2014-15. With the past few months of better jobs data—and upward revisions—we can’t say that any longer.

As you can see in the chart, even with the recent ups and downs in job growth, the broad thrust of the jobs data in 2018 looks better than what we saw in 2016-17 and is comparable to the experience of 2014-15. Within the jobs data, factory job growth continued brisk, and the service sectors, which had languished through most of 2018, have come alive in recent months.

We should throw out the proviso that December data are notoriously volatile because of holiday effects. We abstract from construction and retailing because of their extremely seasonal nature, but the rest of the labor market shows similar—if milder—seasonal swings, which government adjustment procedures don’t always fully capture. And before seasonal adjustment, private-sector jobs excluding construction and retailing rose only 100,000.

Still, any anomalies in today’s data will be ironed out in the next month or two. For now, it is the case that today’s job report was as strong as we have seen in a while, with that strength spread across virtually every sector of the economy.

Our forecast has been for slower growth this year, but no recession. Market sentiment seems to have swung wildly in the past two months, from much more buoyant than ours to much more pessimistic. Today’s data should pull that sentiment back toward the upside.