Press reports this morning have pointed out that much of the October increase in total durables orders came from defense. True, nondefense durables orders rose only 0.1%, and most of the downward revision to September durables orders came within nondefense orders. Nevertheless, nondefense durables orders have at least stabilized over the last five months, after declining significantly over the first five months of 2019. Much the same pattern holds for total durable goods orders. Meanwhile, nondurables orders have risen nicely over the last six months.

I don’t put much store in "soft data" indicators of manufacturing, such as the Institute for Supply Management Index. Such indicators suggest that the US manufacturing sector has fallen out of bed in the last three months. In contrast, "hard data" factory indicators, such as new orders, industrial production, production workers and production hours all indicate that manufacturing began to decline in the fall of 2018, but that this decline bottomed out this past May or June, and there has been some bounce in all of them since then.

This latter seems to me to be the more dependable depiction of manufacturing activity. Certainly, the sector has slowed from the robust growth it saw in 2017 and early-2018, but it is not presently in an ongoing decline that would threaten recession.

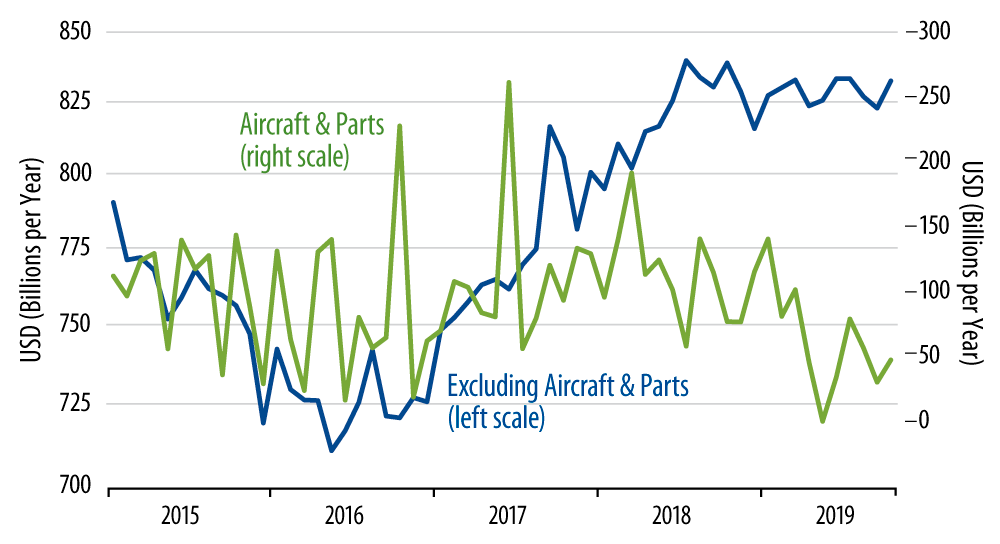

In the accompanying chart, you can see the same story with respect to capital goods orders. After declining from early-2013 through the middle of 2016, CAPEX orders grew strongly from mid-2016 through mid-2018. They then declined in late-2018 and early-2019, but appear to have stabilized over the last six months.

So, if you want to decry this year’s softness in CAPEX as a response to the trade wars or as a sign of impending doom, where were you in 2013-16, when CAPEX orders were declining much more sharply than what we have seen this year? And how do you explain the recent stabilization in both CAPEX orders specifically and factory activity in general? Granted, manufacturing and capital spending could be doing better, but we still have a lot to be thankful for.

In other news this morning, consumer spending grew modestly (but steadily) in October, with both goods and services consumption rising at about the same pace. Core inflation was again weak, as measured by the price index for consumer spending (PCE). Wage income grew strongly in October, but within total personal income, that was partially offset by declines in farmers’ income and interest income, as well as by substantial downward benchmark revisions to past months’ income growth.

Happy Thanksgiving to you, and thank you for reading these commentaries.