2015年11月25日時点

On the eve of the Thanksgiving Day holiday, financial markets were greeted with some decent-to-good economic data. Durable goods orders bounced in October, along with modest upward revisions to September, including similar bounces and revisions in capital goods orders. Personal income rose nicely in October, reflecting the strong October gains in payroll jobs, and there were upward “benchmark” revisions to wage income data going back 6 months. The one downbeat nugget of news was a soft 0.1% October gain in real consumption spending alongside downward revisions to previous months.

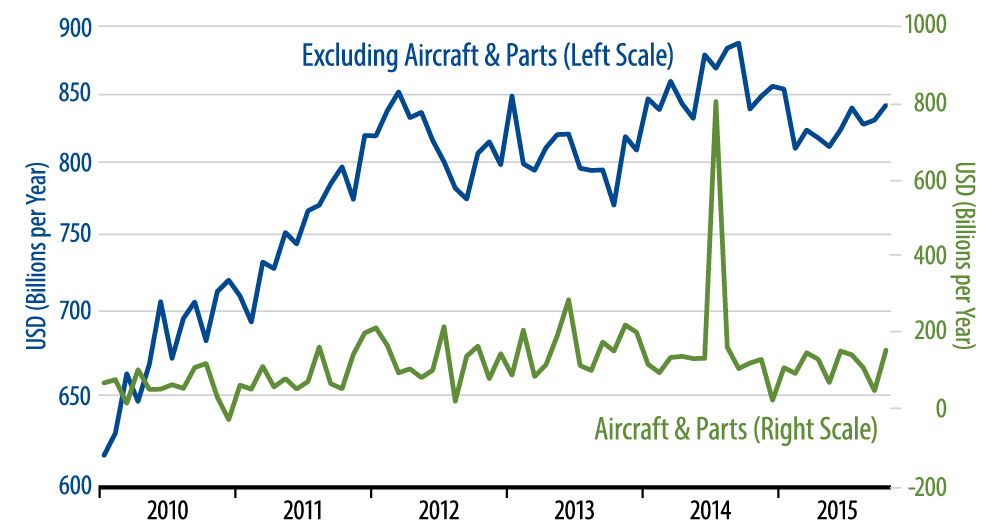

The capital goods data are shown in the accompanying chart. Our forecast line has been that capital spending and exports would stay soft, prolonging the zero-to-slightly-negative growth trend we have seen this year for US manufacturing output. The capital goods orders data have not been in line with that lately, showing a mild bounce, and, indeed, all the factory sector data for October were decent.

Still, the recent bounce in capital goods orders has failed to bring them back to anywhere near late-2014 highs, and the recent bounce has also failed even to challenge the flattish trend of the last four years. Our guess is that the better October factory data are a random “blip,” but, for now at least, they are a blip counter to our forecast line.

By the same reasoning, the recent softness in consumer spending is also likely a blip (downward). Income growth remains decent, and even the softer job growth of July through September was consistent with a decent rate of consumption growth (while the October jobs growth was consistent with stronger spending).

So, all in all, our best guess is that future trends will be continued struggles in the factory sector opposite decent growth in consumer spending, summing to slower GDP growth than what we have seen so far in 2015.