This latter, "core" durables measure has now been essentially flat for the last six months (up at a 0.9% annualized rate), after having risen at a nice, 9.0% annualized clip over the 19 months since September 2016. Other measures of headline durables orders have stalled similarly.

Within durable goods another closely watched aggregate is new orders for capital goods excluding aircraft. That series registered no change in October (-0.04%, to be exact), but its September level was revised by -0.5%.

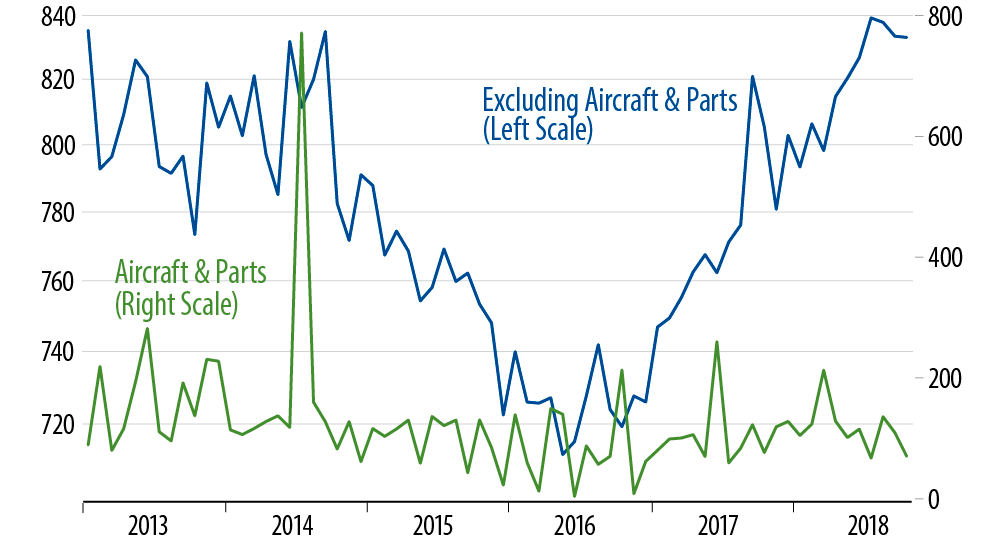

Capital orders have been heading lower for the last three months, not as long-lived a stall as that for total durables and less noticeable than the “head fake” declines observed late last year. (See chart.) This series is volatile enough that the recent declines are something less than decisive. Nevertheless, the recent softness in capital good and in durables in general is concerning.

As we discussed in our "By the Numbers" installment on November 9, all the better US growth of the last two years has come from manufacturing and mining. The manufacturing gains have been driven by capital spending and exports, mining by a rebound in the oil patch. With trade wars darkening the export outlook and with oil prices plunging recently, two of the economy’s recent drivers are in jeopardy, and now the growth in capital spending activity is looking challenged.

Nothing in this picture threatens recession, but it does increase the chances of economic growth slowing to the 2.0%-2.25% range suggested in the aforementioned November 9th installment. Such growth would be below the Fed’s forecasts, and we think it would be a challenge to the pace of rate hikes suggested by recent Fed commentary.