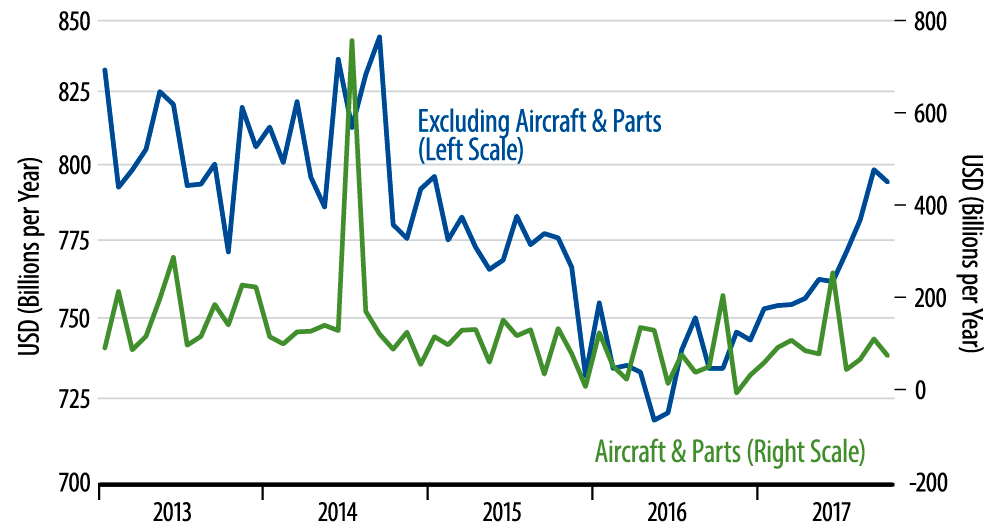

Of special interest within this report are data on capital spending. New orders for nondefense capital goods excluding aircraft declined by 0.5% in October, mostly offset by a +0.4% revision to September’s level. The October declines in CAPEX orders are only a slight offset to very strong September gains, indeed to strong gains throughout the last few months. The accompanying chart tells the story.

There is a lot of month-to-month chop in CAPEX orders, and the declines reported for October are, if anything, smaller than the momentary declines seen during past uptrends in CAPEX orders…and also smaller than the momentary gains seen during downtrends. In other words, there is nothing in today’s data to cast any serious doubt on the uptrend seen in CAPEX orders over the past 16 months.

Given that overall durable goods orders (excluding transportation equipment) showed further gains in October, the uptrend there is even more firmly in place. Meanwhile, it is also clear from the chart that the declines in aircraft orders reported for October are well within the range of the trendless motion seen there for the last three years.

Manufacturing has been the bright spot for the economy this year, offsetting decelerations in both residential and nonresidential construction enough to produce a modest acceleration in overall growth. Given that there has been no pickup in US final demand for manufactured goods outside the CAPEX sector, we have been skeptical that the factory upturn could continue.

Well, the October data for US manufacturing continue to fly in the face of those fears. Factory payrolls, industrial production, and durable goods orders all showed nice gains in October, indicating that the factory upturn is continuing into the fall of 2017.