2015年11月06日時点

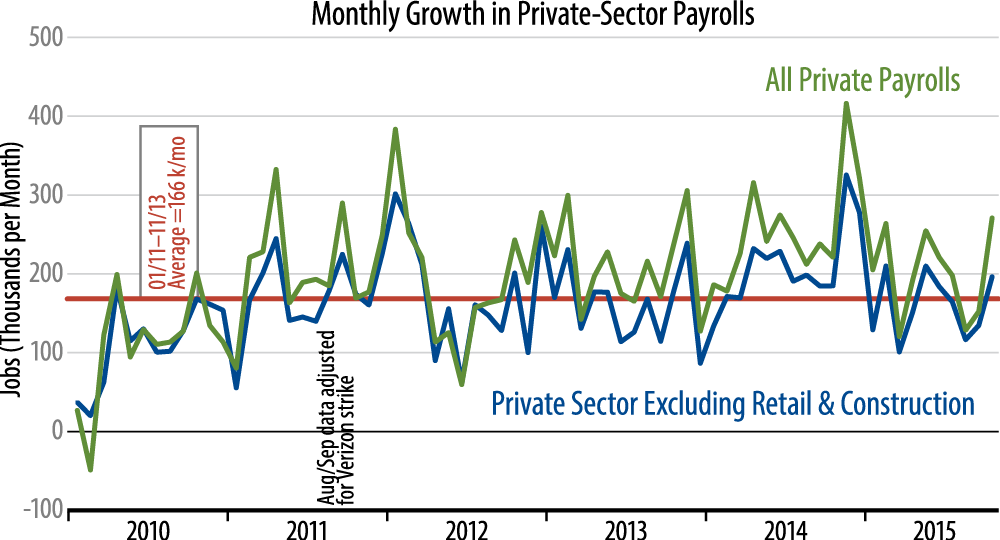

October payroll jobs stunned to the upside today, with private-sector payrolls up by 268,000, and some 50,000 of upward revisions to August and September job gains. As uniformly weak as the September release was, so the October release was uniformly strong, showing good gains in hourly wages (up 0.4% after 0.0% in September), as well as a good gain in construction jobs and some gain in manufacturing, after both sectors had been soft in September.

I’ll stipulate at the outset that today’s news makes a Federal Reserve (Fed) rate hike in December a virtual certainty. A month ago, on the heels of the weak September report, I opined that it would take a strong reversal of that softness for the Fed to hike in December. However, Fed officials and Wall Street analysts then began walking down their estimates of trend growth, claiming that even the soggy jobs gains of late-summer were consistent with full employment and, thus, higher policy rates. Also, Chairperson Janet Yellen’s comments of recent weeks indicated an intent to tighten in December. Then, after all that walking back and “battlefield preparation,” we get a release today that reverses much of the previous softening.

So, a Fed move in December is a pretty sure thing, though it is still likely that such a move—and any successors—will be delivered so as to minimize its impact at the long end of the curve or on the stock market. The Fed does not want to slow down growth nor disrupt the markets.

Aside from Fed implications, today’s news was less consequential than the headlines suggest. As seen in the accompanying chart, even with the stronger October data and upward revisions, there is still a clear 2015 slowing in job growth compared to 2014. This slowing is even more apparent in the household job series (whence the unemployment data are derived) and when 3- or 6-month averages of these series are plotted.

Finally, while factory jobs did show a minor gain, my guess is still that the ongoing 2015 downtrend in US manufacturing activity is still in place.