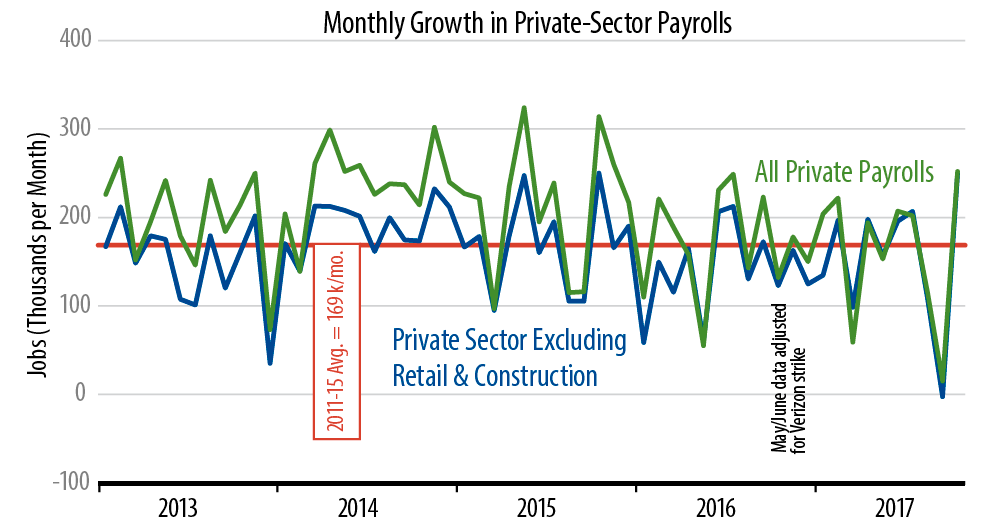

As robust as these gains sound, it is worth emphasizing that they only partially offset the weakness seen in September related to hurricane effects. You can see this visually in the accompanying chart. Find the point midway between the abysmal September gains and the “robust” October gains, and you will see that that midpoint is below the prevailing trend growth rates for both series shown in the chart.

In terms of the numbers, our favored payroll measure shows an average gain of 123,000 over the last two months (a 3,000 job loss in September offsetting most of the 249,000 gain for October), which on average is well below the 169,000 average gains this series shown over 2011-15. As we have remarked continually in our installments of “By the Numbers,” job growth has slowed over the last two years, not dramatically, but enough so that claims of accelerating consumer spending to come are far-fetched. No matter how buoyant the stock market is, consumption is quite unlikely to speed up when job growth and income growth are slowing down.

In line with that thought, hourly wage data for October showed a slight decline, effectively negating the apparently strong wage gains shown for September. A month ago, we thought those wage data were just as distorted as the jobs data. Because low-wage workers were more likely to be “off payroll” in the Gulf Coast states due to the hurricanes, the average wage data for September were biased upward. Today’s news supports this contention. Averaging the September and October wage gains together, hourly wages for production workers have risen at only a 2.4% rate over the past six months, compared with 2.7% growth this time a year ago. Similarly, hourly wages for all workers have grown at a rate of 2.7%, compared with 2.8% growth this time a year ago.

It could be that there are still some hurricane effects in these data. We’ll find out next month for sure, but in the meantime, the payroll data on most counts belie claims that the economy is accelerating.