The September gain in headline sales was driven by an incentive-induced bounce-back in car sales and hurricane-driven increases in gas prices. So these factors didn’t affect “control” sales, which showed decent but more modest gains in recent months.

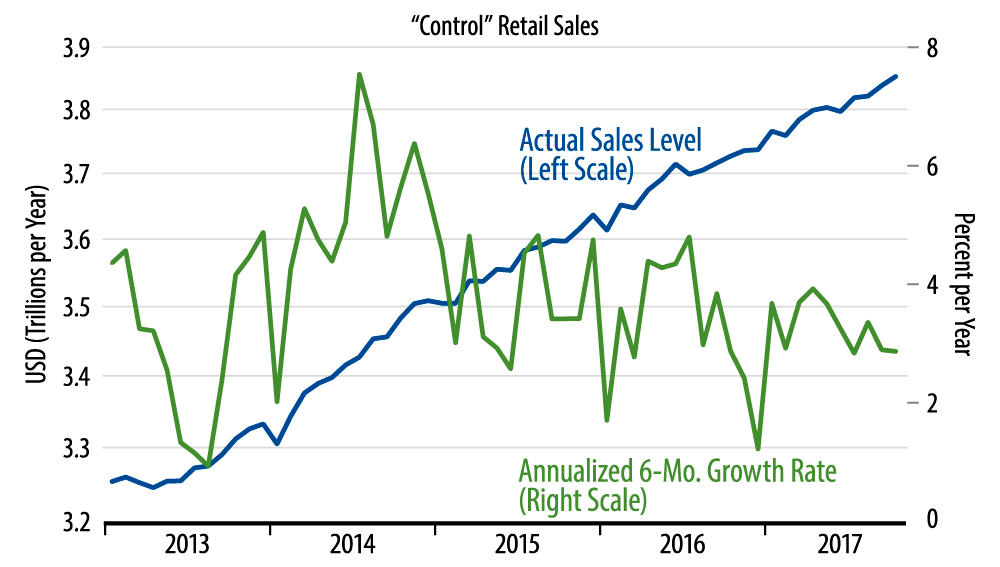

As seen in the accompanying chart, sales growth has been generally steady for quite some time, with six-month growth rates for control sales stuck around the 3.4% rate for most of the last two years. 3.4% is actually a pretty decent rate of growth, but the steadiness of this pace belies claims that the economy is accelerating.

We will admit that capital spending has looked better lately, but that has largely been offset by slower growth in both residential and nonresidential construction. So the 3% GDP growth seen over the last two quarters is partly a bounce-back from a sluggish 1Q17 rate and partly due to a surge in inventories. We do not expect the inventory surge to continue, and it may even be reversed in coming months. In any case, there is no sign of an acceleration on the consumer spending front.

While aggregate sales growth was in line with preceding trends, store-type details provided an interesting contrast with recent experience. Sectors that had been soft showed nice gains, such as grocery, apparel, electronic, and book/sporting goods stores. At the same time, sectors that had been doing well saw sales declines, namely the high-flying online sector, but also building materials stores. Is this a sudden divergence in retail trends or merely a random blip? Our money is on the latter explanation, but we’ll wait for coming months’ data to tell us for sure.