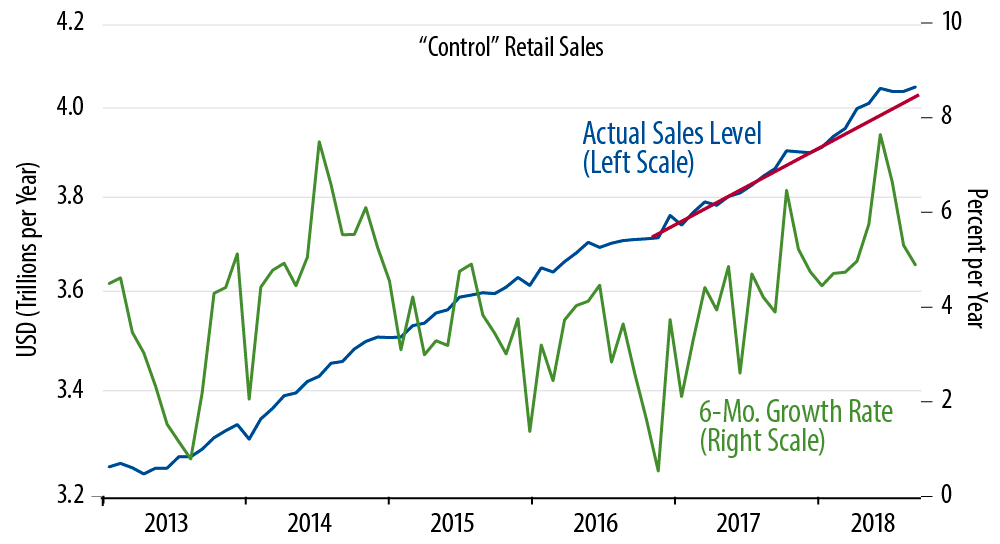

The accompanying chart tells the story. Control sales had bounced in May and again in July, pulling sales levels above previous trends. However, the moderation over the last three months has brought sales levels almost all the way back to that "previous" trend line. The six-month growth rate for control sales now stands at 4.9%, up only marginally from the 4.0% trend growth seen in 2017. In other words, the May/July burst in sales has fizzled much as did the burst seen in November 2017.

Sales at most store types were nondescript. For those store types seeing nice October gains, such as vehicle dealers, building materials stores, and clothing stores, those gains just offset—or mostly offset—sales declines in preceding months.

No, sales are not weak. 4% to 5% sales growth leaves 3% to 4% real growth after adjusting for prices. However, much of that growth in consumer spending on goods is going to imported goods, leaving little net boost to the domestic economy. Meanwhile, the other 69% of consumption, spending on services, continues to chug modestly and steadily, showing none of the frothiness evinced by retail sales in May and July (let alone in November 2017).

Overall, the consumer is doing okay, but there is little or no evidence of an acceleration in consumer spending that would drive faster aggregate economic growth. These data are consistent with the 2.0%-2.25% GDP growth expectations laid out here last week.