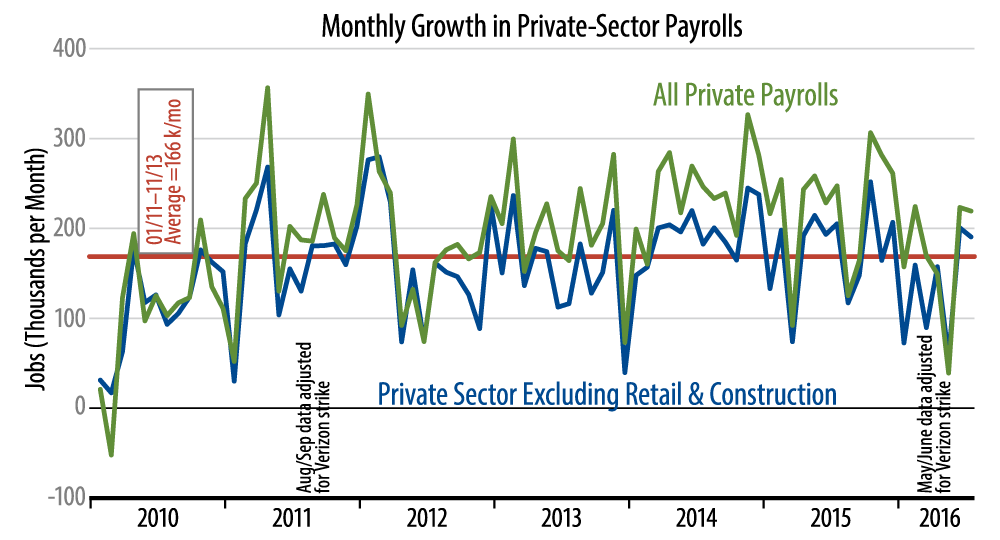

Private-sector payroll jobs rose by 217,000 in July, sustaining the better growth of June, following softer data for the 5 five months of the year. The "core" measure we track, which abstracts from especially volatile construction and retailing sectors, grew by 217,000 in July, following a gain of 221,000 in June. As seen in the accompanying chart, both of the last 2-month's gains were well above the 166,000 per month average of recent years for this measure, and they were also a marked improvement from the pace of the first 5 months of 2016.

As discussed in previous installments of By the Numbers, slow job growth through May was mostly focused in manufacturing and in industries that complement manufacturing, such as mining, logistics and professional services. All of these industries showed better job growth in July, with the exception of mining. The gains in factory production jobs and production hours worked were not sharp, which is to say they do not clearly break the downtrends that factory payrolls had been suffering through, but they were a start.

Elsewhere in today's news, household (within the unemployment dataset) showed a strong gain of 420,000, following essentially zero change over the previous 4 months. A similar-sized increase in the labor force kept the unemployment rate from dropping in July, but here too there was better news after a run of softer data in previous months.

The data today pose something of a dilemma for the Fed. Payrolls improved over the last 2 months, but they don't fully offset softer growth over the preceding 5 months. The improvement in manufacturing is tentative at best, and last week’s news puts real GDP growth at only 1.2% for the last 4 quarters, way below the Fed’s forecast. In other words, there is some fodder today supporting a rate hike, but it is balanced by less encouraging data previously. Most likely, it will take further good news on jobs and production in August for a rate hike in September to be on the table.