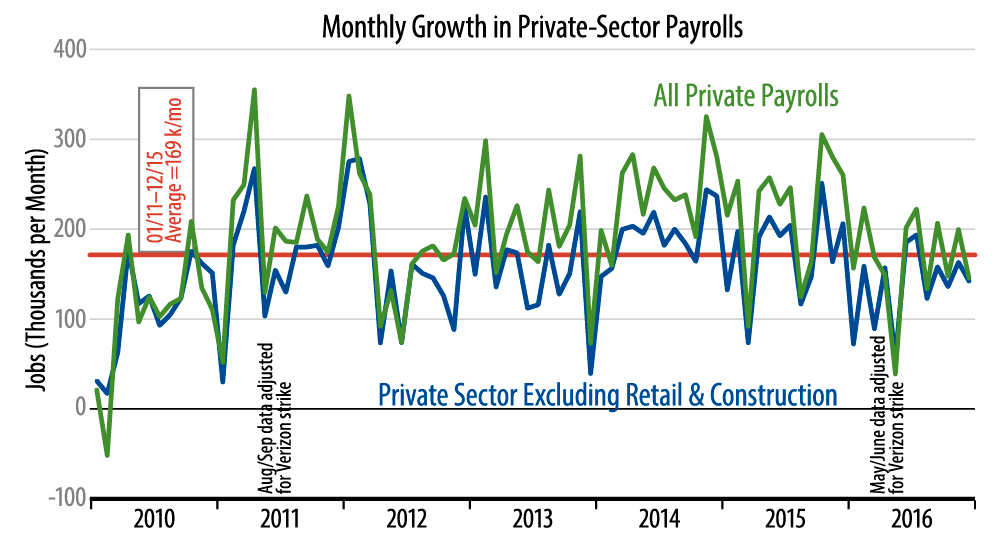

To make this point more explicitly, we can point out that for all of 2016, total private-sector jobs rose by 164,500 jobs per month on average, compared with average rates of 240,000 in 2014 and 220,900 in 2015. Our core measure showed average growth of 134,600 jobs in 2016, compared with 192,800 in 2014 and 172,600 in 2015.

Now, it is true that the gains of 2014—and possibly those of 2015—were boosted by the expiration of extended unemployment benefits on January 1, 2014, an expiration that is estimated to have pushed 2 million non-employed benefit recipients back into the labor force. Still, the fact remains that underlying job growth—and economic growth with it—has been decelerating steadily for the last two years. Many market pundits allege that the economy was picking up steam in late-2016, but their most cherished measure, payroll job growth, belies this contention.

Of course, the spin will be that recent job gains are all that is necessary to sustain supposedly full employment. The other side of the coin is that the rate of gains in payroll jobs has been decelerating for the last two years, and it is not obvious that this deceleration has been arrested. So, Mr. Trump and friends have a lot of work to do in their efforts to revive economic growth.