The November gains were distorted a bit by the resolution of the GM strike. That dislocation caused a temporary job "loss" of -40,000 in October, as we commented in this space last month. So, the November gains were overstated by the return of these 40,000 striking workers to the payrolls.

Even so, the November job gains were impressive, especially so given that the ADP survey released on Wednesday showed a gain of less than 70,000 jobs. We always say survey data can be misleading, and we’ll have more to say on that shortly.

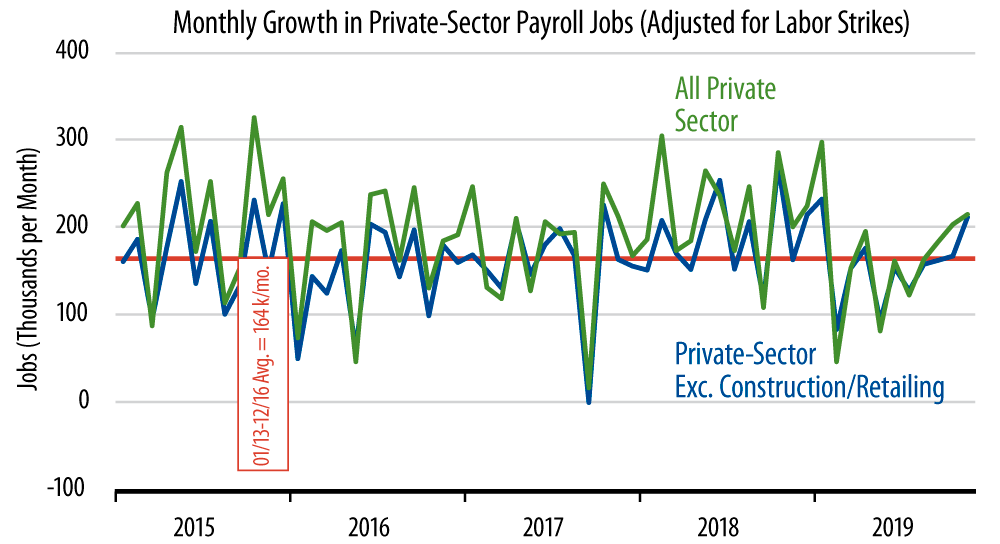

The accompanying chart shows the latest data adjusted for the GM strike in October, as well as for the Verizon strike of May 2016. As you can see there, the (adjusted and revised) job gains of September and October had gotten the economy back to the average pace of recent years, after a stumble early this year. The November job gains were well in excess of that average.

Also reassuring was a gain of 54,000 in manufacturing jobs. Upon adjusting for the GM strike, that gain shrinks to 14,000, but that is still a solid gain on the month. These readings stand in stark contrast to the latest report on the manufacturing ISM index, which declined further in November.

In recent posts, we have pointed out that the "soft data" ISM declines of September and after have been accompanied by marked stabilizations or improvements in all the "hard data" measures of factory activity. Factory jobs are one such hard data indicator. Factory production worker employment had declined early in 2019, but has rebounded a bit in recent months. Our thinking is that the ISM readings are either wrong or else are depicting what the factory sector was doing four to six months ago, NOT presently.

All in all, today’s data were an early Xmas gift to those looking for decent to good performance in the US economy. All of us here at Western Asset hope your holiday season is similarly cheery.