2015年03月06日時点

Headline payroll jobs showed a strong increase in February, with total jobs up 295,000 and private-sector jobs up 288,000. There were mild downward revisions to the January gains, but those still left a strong increase of 1,258,000 over the last four months together.

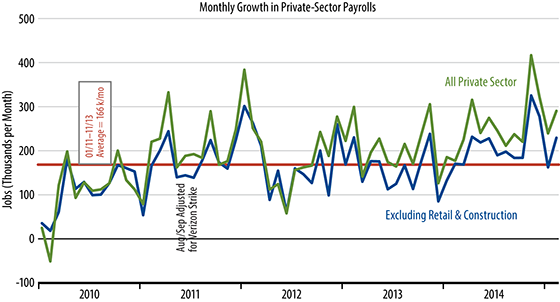

The accompanying chart shows monthly gains in the two series we regularly focus on in these commentaries: total private-sector jobs and private-sector jobs excluding construction and real estate. This latter series is especially relevant presently given the seasonal fluctuations that construction and retailing always undergo this time of year. Net of those seasonal sectors (blue line), job growth was above-trend in February, after falling slightly below trend in January, and that after very strong gains in November and December. So, even without construction and retailing, there has been a substantial pick-up in job growth over the last four months, following five years of slower trends.

Has the economy picked up in line with the job growth acceleration? Well, there hasn’t been any sign of that yet, although it is too early to tell for sure. Output and spending numbers show little net change in recent months, even before any effects of severe winter weather. While the response of economic output is still unclear, job growth itself surely has been stronger of late, and we have the markets moving today in response to that.

In another sign of recovering labor markets, the “employment rate” (also known as the employment-population ratio) rose again to 59.3%, bringing it almost back to the 59.4% rate of 2009 at the start of the expansion. It is still way below the 63.4% rate that held at the outset of the recession in 2007, but there has been a marked improvement there over the past 18 months.