Our control sales measure excludes car dealers—as well as building materials stores and service stations—thus providing a better measure of "underlying" sales growth. It showed a gain of 0.38% in March, but with a -0.13% revision to February. On net, control sales in March were up 0.26% from what was previously announced for February.

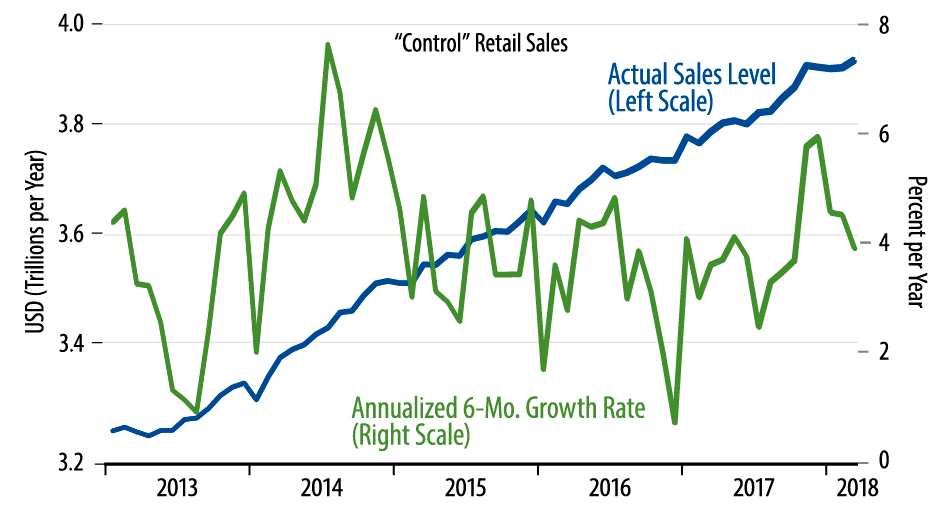

The accompanying chart tells the story. Today's data break the string of declining sales over the previous three months. However, they do little more than continue sales at the same underlying growth pace as we have seen for the past three years. This conclusion is echoed by the six-month growth rate for control sales also seen in the chart, which is likewise now back to its levels of the past three years.

The last few months' retail sales data provide a good Rorschach test of one's views. When retail sales showed explosive growth last November, the consensus view was quick to label that as the first evidence of the consumer upsurge they expected. For the last three months, those supporting this view have been groping for reasons why spending was so "anomalously" slow. Early indications are that they are touting today's "strong" gains as vindication of their expectations.

My own take was that the November gains were a one-time Christmas binge, so that the three months' declines seen through February were merely a return to trend. Today's data merely show a continuation of that pre-November trend growth. Why lock on a one-month gain that has since been reversed, and why lionize a March gain that is distinctly mediocre? Ask them.

On net, todays data do not move the needle for economic growth. I look for 1Q18 GDP to come in at about 1.5%, with real final demand growing less than 1%. We’ll see how the actual estimates turn out in our next installment on April 27.