Leading the October sales rebound were nice gains in sales at building materials, clothing and grocery stores. Each of these sectors had shown sluggish sales growth through much of 2016, but enjoyed a bounce in October. On the other side of the ledger, sales at restaurants, electronics stores and department stores continued to see varying degrees of sluggishness. Online sales, which had been hot early in the year before cooling slightly in summer, saw a renewal of strong sales growth in October.

While it is a major element of the economy, consumer spending has been something of a reverse indicator in 2016. It was strong in the first half, when GDP growth was weak, then it slowed considerably in the third quarter, when GDP growth was reported to be stronger. Today’s consumer spending data suggest something of a rebound in the fourth quarter.

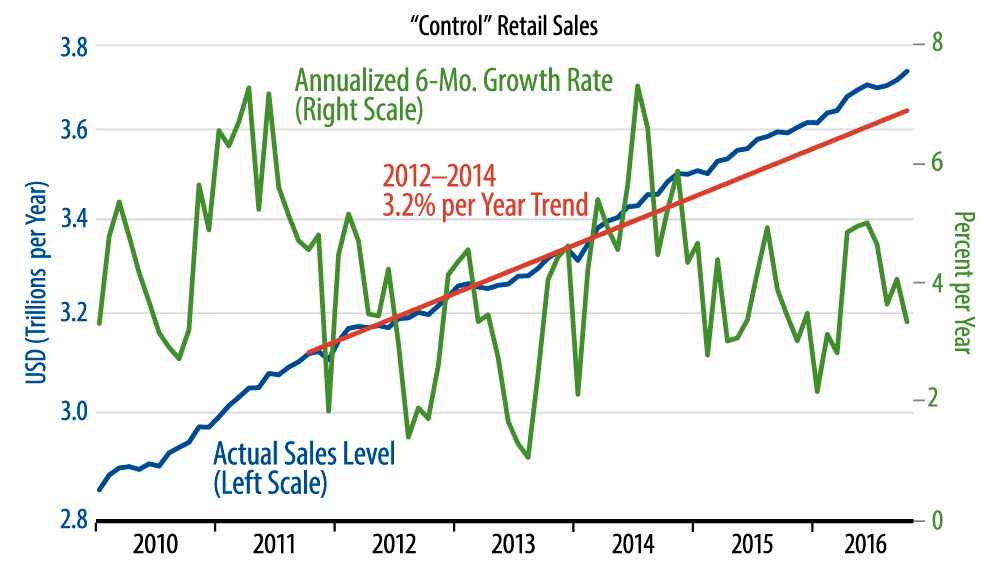

As seen in the accompanying chart, retail sales growth moved considerably above 2012–14 trends in 2015 and early-2016, but has reverted to trend growth recently. Folding in October growth with that of the spring and summer, we have recently seen an underlying growth rate for sales of around 3.3%. This should quash fears of a significant slowing in consumer activity, but it is not sufficient to singlehandedly drive a sustained upturn in overall growth, especially given ongoing sluggishness elsewhere.

Meanwhile, market reaction over the last week to the election of Donald Trump has certainly run counter to our expectations of continued sluggish growth and stable interest rates. We acknowledge that drubbing, but we would also predict that the road to a stronger economy is trickier and more drawn out than that market reaction would suggest. We’ll have more to say on this in future installments.