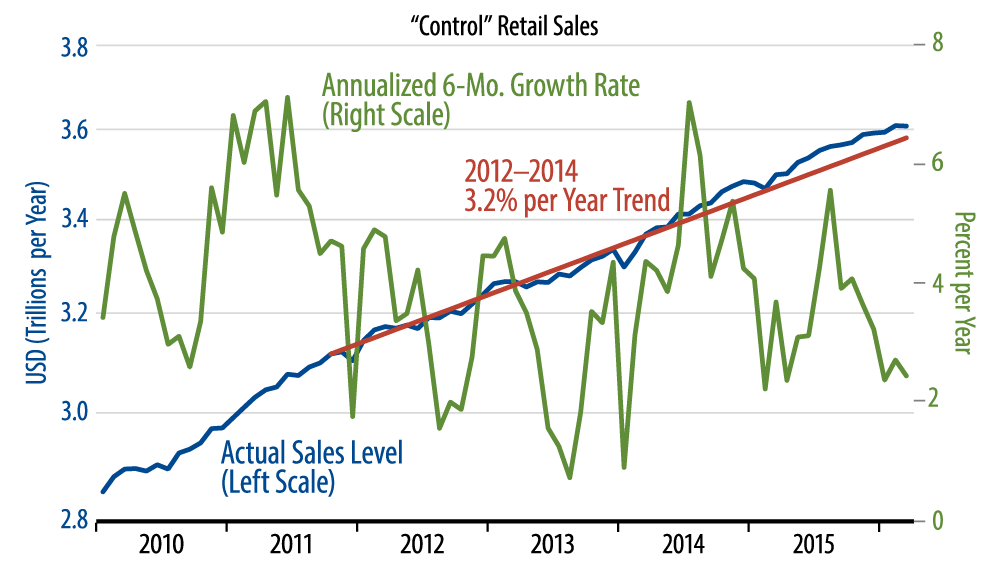

Retail sales came in below expectations yet again in March, dashing hopes—for now—of a consumer upturn that would pull the US economy back above 2% GDP growth. Headline (total) sales showed a 0.3% decline, although February sales were revised up 0.2%. Looking at "control" sales, that is excluding volatile car, gasoline and building materials stores, sales were essentially flat in March (down 0.03%), but there was a 0.4% upward revision to February.

In other words, sales growth was not horrible over February/March, but it showed no sign of the acceleration that various Wall Street commentators and Federal Reserve policymakers were looking/hoping for. This depiction is echoed in the chart. After moving above trend in mid-2015, control sales have been drifting back toward pre-2015 trend lines for the last 8 months, showing little more than 2% annualized growth over that span. Even allowing for the fact that retail prices are generally declining, this pace is less than exciting, but there are no declines that would give one reason to be fearful of a recession.

Within individual store types, the only counter-note to this trend is substantial recent sales growth at building materials stores. At all other major store types, sales have turned sluggish in the last few months, with the softest performance at car, furniture and apparel stores.

In sum, the soft March retail sales report is a blow to those projecting an acceleration in US GDP growth back to the 2%-2.5% range that held prior to 2015. It is right in line with our forecast, which is looking for slower growth, say about 1.5%, thanks to the continuing problems in US manufacturing.