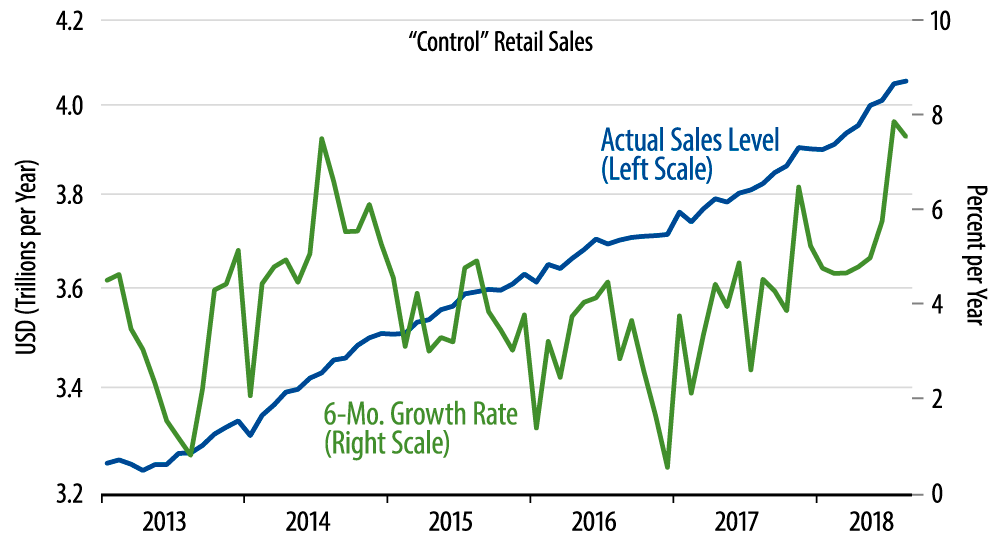

The July gains were already looking robust, and the revisions to those numbers make it look even better. So, it is indeed the case that the revisions to July make up for the softness in August sales growth. As you can see in the accompanying chart, thanks to robust sales gains in May and July, underlying sales levels have moved above their preceding growth trends in the last few months.

Our take has been that the July spike in sales was a "one-off" phenomenon, similar to the spike seen in sales in November 2017 (that was reversed in the subsequent three months). The numbers since then have not been affirmative on this take. While sales growth in June and August was soft, the sales gains in July, again, were almost as strong as those of May. So, if nothing else, we haven’t seen the quick reversal of May gains the way we did six months earlier. We are not yet abandoning our take that retail sales growth will revert to pre-May trends, but is in jeopardy after the news of the last four months.

In terms of individual store types, restaurant sales spiked through July, powering much of the strength in overall sales then. Restaurant sales rose 0.2% in August, so while the August growth there was not strong, there was no reversal of the very strong gains there over the previous three months. Meanwhile, sales in other store types were less spectacular, with sales declining at apparel stores, furniture stores, building material stores and motor vehicle dealers. The latter two store types are not included in control sales, because businesses buy from these stores as well as consumers, but the declines there and elsewhere suggest that consumers are being discriminatory, even as they open their wallets a bit.