2014年2月13日時点

As we see it, the best chance for faster US growth (and higher bond yields) in 2014 resides in a continuation of the strong growth in retail sales and housing starts seen at the end of 2013. If retail sales continue to grow at their 4Q13 pace and if homebuilding accelerates to levels consistent with the November and December housing start prints, then 3% or better real GDP growth would indeed be very likely. The problem is that there were suspicious elements to both of these upturns; 4Q13 retail sales growth was much faster than is consistent with accompanying growth rates in personal income and services consumption, and housing starts were dramatically higher than what was indicated by recent building permit and new-home sales levels.

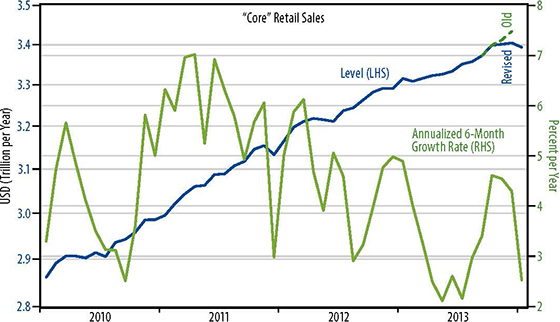

So, today’s retail sales release provided an important look at how retailing started the year. (We’ll see about housing next week.) The accompanying chart shows levels and growth rates for the "core" retail sales measure we track most closely. As with the core jobs number analyzed last week, this sales measure abstracts from especially volatile retail sectors and also homes in on those retail sectors most reflective of consumer demand.

In looking at this chart, you might be asking, "Where is that 4Q13 retail surge he’s talking about?" The answer is that the Census Bureau has revised it away! Previous data had shown sales growth at an annualized rate of 7% or better in all three months of 4Q13 (dotted line in chart). Current, revised data now show essentially zero growth in November and December, followed by a 0.3% decline in January.

Surely, the January decline could be weather-induced. However, that does not diminish the fact that the 4Q13 retail surge now looks to be a one-month (October) wonder, much as we expected.