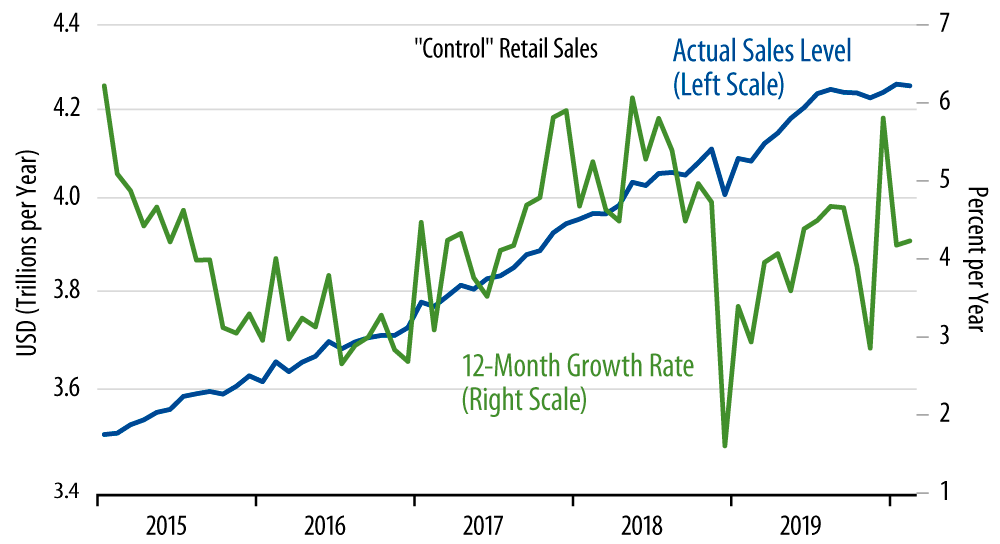

In the meantime, there was a data release today, with February retail sales. These showed a -0.5% decline in February, offset slightly by a +0.2% revision to the January estimate. Our control sales measure, sales excluding those at vehicle dealers, building material stores, and service stations, declined a slight -0.1%, with an offsetting +0.1% revision to January.

So, retail sales continued to be soggy in February, for the sixth straight month (see chart). As we have remarked in past installments covering retail, this sogginess doesn’t make a lot of sense, given that consumer incomes have been growing as strongly as ever and that consumer spending on services has continued to grow with no let up at all. We saw a similar "pause" in retail sales a year ago that stretched from July 2018 through February 2019, which is why the 12-month growth rate shown in the chart has held up so well.

We could further ponder the import of this retail sales pause, except that it has been overtaken by recent events. That is, the cause of this pause—be it bad data or some other fluke—vanishes in significance against the possible hit retail sales and all the other indicators now face given the widespread quarantines and work stoppages being mandated presently in order to contain COVID-19. If retail sales could fall to zero growth for six months alongside no detectable decline in consumer activity, imagine how they could fall with large proportions of the population stuck in their homes.

As dramatically as the economic data might change in coming weeks, keep in mind that the full hit to these indicators won’t be reflected until the April data to be announced two months from now. Even then, the news most likely to be driving markets and politics will be the infection counts, which we all will be watching for signs of inflection, deceleration and a topping out.

In the meantime, we expect to be here, analyzing the data announcements for what they are worth. We will try to stay well, and we hope you do the same.