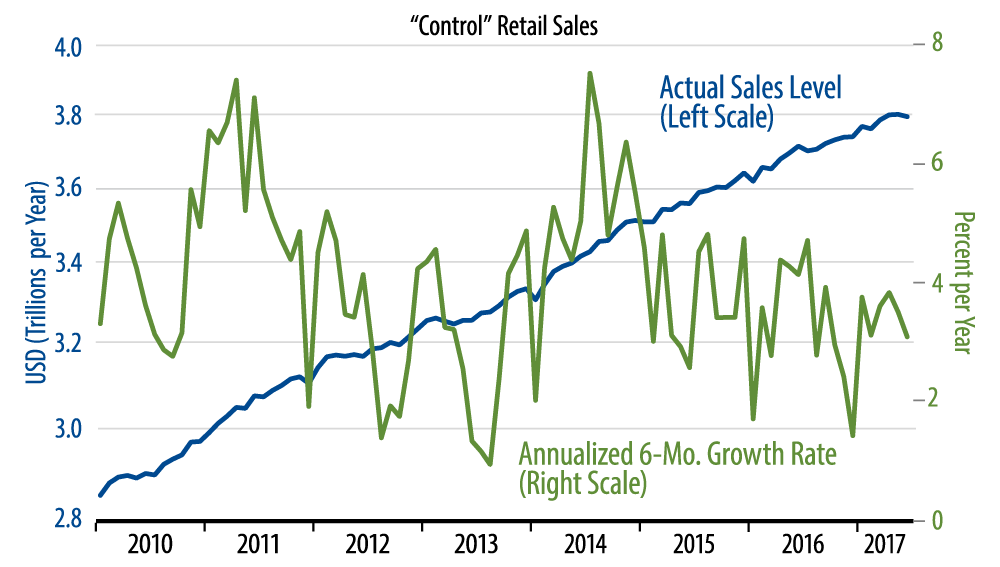

Retail sales have been lackluster virtually every month so far this year, but the softness over the last two months has been especially noticeable, as the accompanying chart makes clear. Our core sales measure shows 3.1% annualized growth for 2017 through June. This is not horrible, but it clearly is not the acceleration that much of the Street has been calling for.

The Street has been expecting stronger sales growth because of the low unemployment rate and rising stock market. Our counter has been that despite low unemployment, actual job growth has been slowing since early-2016, and wages have been decelerating over the past year, so that wage income growth has decelerated markedly, which, in our view, precludes a consumer upturn. So, we do not find the sluggishness in consumer spending for 2017 to date surprising.

In terms of store types, sales growth has been slowing this year at restaurants, grocery stores, book and sporting goods stores, furniture stores, building material stores, car dealers, and apparel stores. There have been mild upturns in sales at electronics stores and department stores, while online retailers (nonstore retailers) have seen steady growth.

Again, the consumer is steady at best or slowing somewhat, at worst. We continue to think that the main swing factors for the economy through the rest of 2017 will be capital spending, exports, and single-family housing, and we expect softer growth on all three counts.