2014年8月28日時点

We were on vacation a month ago when the U.S. Department of Commerce (Commerce) first released data on 2Q14 GDP and benchmark revisions to prior years' data, but we can cover that news in the context of today's monthly revisions to 2Q14 GDP. Every month, Commerce revises its current-quarter GDP estimates, as more complete survey data come in for the various components of GDP. Once a year, in July, Commerce introduces “benchmark” revisions that change GDP estimates back a number of years. These benchmark revisions incorporate information from annual tax returns and censuses of manufacturers, retailers, etc.

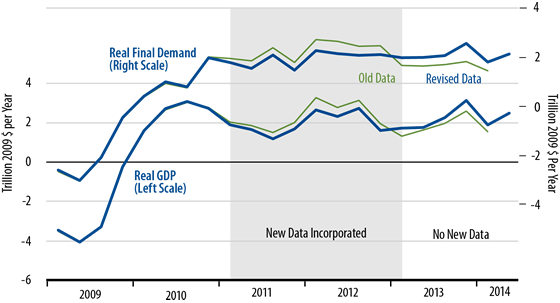

A month ago, headlines emphasized upward revisions to GDP growth over the last year and a robust-sounding 3.9% growth rate in 2Q14. What garnered less attention were downward revisions to growth over 2011 and 2012, large enough that the level of 4Q13 GDP was actually revised by -0.2%. You can make your own sense out of the fact that the upward revisions to GDP growth occurred over a period (2Q13 and later) when Commerce really had no new information to incorporate into the data, since the new tax return and census data essentially concern 2011 and 2012.

The benchmark revisions—along with today's revision of 2Q14 GDP from 3.9% to 4.2%—put growth over the last four quarters at 2.5%, a bit of an improvement from the 2% trend of recent years. As the accompanying chart makes clear, that acceleration in GDP growth is largely due to faster inventory accumulation. Real final demand (GDP less inventory investment) shows growth over the last four quarters of 2.2% essentially unchanged from preceding trends.

The revisions do portray final demand growth as steady, rather than the apparent, slight deceleration that the prior data showed. Still, steady growth is not an acceleration, and there is little in these data to give succor to Federal Reserve (Fed) forecasts of steady 3% growth. Inventory accumulation is unlikely to see further bursts, so demand growth is going to have to accelerate substantially to fulfill the Fed's forecast.

What about 4.2% growth in 2Q14? That is clearly payback from a weather-restrained -2.1% decline in 1Q14. Average them together, and both GDP and final demand are showing growth of less than 1% year-to-date, without weather as a factor from 4Q13 to 2Q14. We do expect a better pace in the second half of this year, but not enough to establish a 3% growth trend.

The catch-up nature of 2Q14 data is reflected in corporate profits. While domestic profits rose +9.7% in 2Q14, that was not enough to fully offset a -10.2% decline in 1Q14. On net, over the last four quarters, domestic profits are down by -0.9% and total global profits of domestic corporations are down -0.3%.