For the year-to-date, industry in general and manufacturing in particular had been the only bright spots in an otherwise middling 2017 growth story. Services have been flat this year, and construction has been weakening, but manufacturing and oil production had shown nice increases, with the former’s gains coming after four years of zero growth.

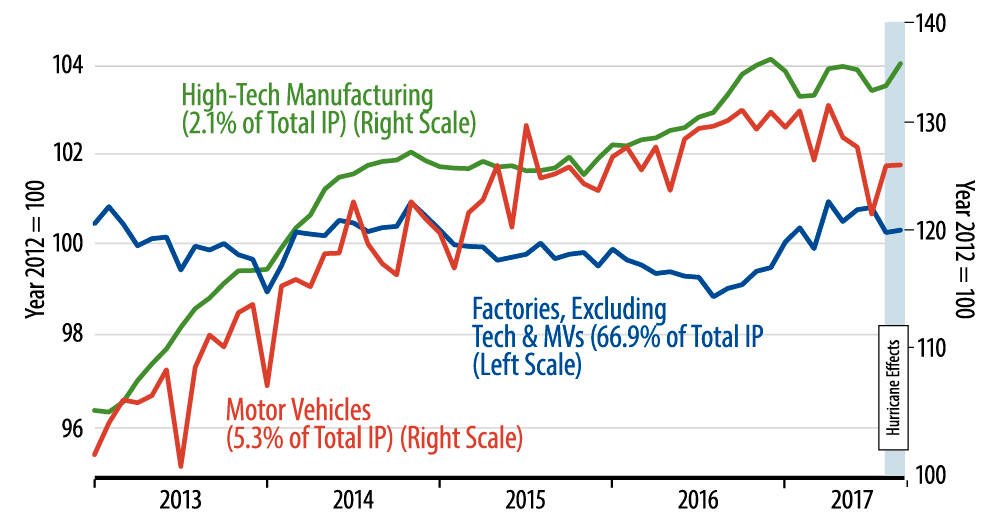

Today’s sluggish performance for manufacturing raises the question of whether the 2017 upturn will be sustained. Yes, hurricanes can be blamed for the especially weak performance in August and September. However, as seen in the accompanying chart, thanks to the data revisions, manufacturing excluding tech and vehicles now looks to have been soft since April (blue line), so there is more than just the hurricanes driving the softening.

Meanwhile, the motor vehicle sector has been flat for two years and declining since this past winter (red line). Tech sector output has been flat all year (green line), and even the growth it showed in 2016 was but a pale image of the robust gains this sector had shown in prior expansions. Meanwhile, oil production rose again in September, but oil rig drilling declined for the third straight month (neither shown in the chart).

We have not been “buyers” of the contention that the US economy has been improving recently. Industrial activity had been the one sector supporting the improvement claims, and lately even that sector has soured. We will get some bounce in industry in the next few months as the apparent hurricane effects subside, but it will be interesting to see just how much bounce actually occurs...and how much of the softening apparent since April remains in the data.